6-1

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

chapter

6

Accounting for

Merchandising Businesses

_____________________________________________

OPENING COMMENTS

Chapter 6 introduces the merchandising form of business. It opens by contrasting the income statements

of service and merchandising businesses. The majority of the chapter is focused on the presentation of

inventory, purchase of inventory, and sale of inventory including returns, discounting, and freight

charges.

The 27th edition of Accounting focuses on the perpetual inventory method, since computerized

accounting and inventory systems have made it feasible for even small merchandisers to track each

purchase and sale of inventory. The text illustrates how to record transactions related to the purchase and

sale of merchandise under the perpetual inventory system. It also presents a chart of accounts and an

overview of the accounting cycle for a merchandiser using a perpetual inventory system. The chapter then

presents the financial statements for a merchandising business and summarizes the essential differences

between the periodic and perpetual inventory systems.

A summary of the closing process as it differs in a merchandising environment is provided to assist

students in identifying additional income statement accounts to include in the closing process.

A presentation of the asset turnover that illustrates how effectively a business is using its assets to

generate sales follows and explains its relevance to a company from year to year or as a comparison to its

industry average.

The appendix explains and illustrates the use of the periodic inventory system. It also contains a table that

displays how the same business transaction would be journalized differently between perpetual and

periodic inventory systems.

6-2 Chapter 6 Accounting for Merchandising Businesses

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

After studying the chapter, your students should be able to:

1. Distinguish between the activities and financial statements of service and merchandising

businesses.

2. Describe and illustrate the accounting for merchandise transactions.

3. Describe and illustrate the adjusting process for a merchandising business.

4. Describe and illustrate the financial statements of a merchandising business.

5. Describe and illustrate the use of asset turnover in evaluating a company’s operating

performance.

KEY TERMS

administrative expenses (general expenses)

asset turnover

cash refund

cost of merchandise sold

credit memorandum (credit memo)

credit period

credit terms

customer allowance

customer discounts

customer refunds payable

debit memorandum (debit memo)

estimated returns inventory

FOB (free on board) destination

FOB (free on board) shipping point

gross profit

income from operations (operating income)

inventory shrinkage (inventory shortage)

invoice

merchandise inventory

multiple-step income statement

operating cycle

other expense

other revenue

periodic inventory system

perpetual inventory system

physical inventory

purchases discounts

purchases returns and allowances

sales

sales discounts

selling expenses

single-step income statement

trade discounts

wholesalers

Chapter 6 Accounting for Merchandising Businesses 6-3

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

STUDENT FAQS

How do you handle a business that is primarily a service business but has some merchandising

aspects?

In a merchandising (retail) type business, how can you use the periodic inventory method and still use

a computer to monitor inventory?

Which method is more current or is more correct so that what is in inventory can be determined at any

given time?

When viewing a chart of accounts, how can you determine if it is for a periodic or perpetual inventory

system?

What accounts are in the chart of accounts of a periodic inventory system?

What accounts are in the chart of accounts of a perpetual inventory system?

Which inventory method will yield the most net income?

Which inventory method will yield the least net income?

How can a business have gross profit but end up with a net loss for the year?

Why not debit the sales account directly for any adjustments?

Why do you add transportation in and do not deduct delivery expense when determining the cost of

merchandise purchased?

Why does it matter that we identify other revenues and expenses on the income statement? It doesn’t

impact the overall net income or net loss.

Why can’t we deduct credit card expense from sales? After all, it reduces the cash we receive from

the sale.

Why don’t discount terms apply to the total amount we may owe a supplier when the supplier prepays

the freight for us?

Why do we record the sales tax separately from the sales amount? Wouldn’t it be easier to credit

Sales for the total amount (sales and tax) and then debit Sales when we remit the sales tax?

When computing asset turnover, why is there a choice about which value of assets to use? Does it

matter?

OBJECTIVE 1

Distinguish between the activities and financial statements of service and merchandising

businesses.

SYNOPSIS

The differences between service and merchandising businesses are discussed in this chapter. The first

objective describes the operating cycle process for merchandising businesses in Exhibit 1. The time in

6-4 Chapter 6 Accounting for Merchandising Businesses

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

days of this operating cycle differs vastly depending on the type of merchandise sold. Financial

statements reflect the differences between these types of businesses. The income of a services business is

often reported as fees earned; for a merchandising business, it is reported as sales. Condensed income

statements from a service business (H&R Block) and a retail business (The Home Depot) illustrate how

these statements differ.

Key Terms and Definitions

Cost of Merchandise Sold - The cost that is reported as an expense when merchandise is sold.

Gross Profit - Sales minus the cost of merchandise sold.

Merchandise Inventory - Merchandise on hand (not sold) at the end of an accounting period.

Operating Cycle - The process by which a company spends cash, generates revenues, and

receives cash either at the time the revenues are generated or later by collecting an accounts

receivable.

Sales - The total amount charged customers for merchandise sold, including cash sales and sales

on account.

Relevant Example Exercise and Exhibit

Exhibit 1 – The Operating Cycle for a Merchandising Business

Example Exercise 6-1 – Gross Profit

SUGGESTED APPROACH

The goal of Objective 1 is to introduce the student to the basic skeleton of the income statement for the

merchandiser.

Sales

– Cost of Merchandise Sold

Gross Profit

– Operating Expenses

Net Income

To demonstrate the need for this new format, ask your students the following question: What is the largest

expense incurred by a retail store, such as Target or Old Navy? (Answer: the cost of the merchandise that

is sold to the customer)

Because this cost is the retailer’s major expense, it is shown separately from the operating expenses when

preparing the income statement. The cost of merchandise sold is deducted from sales to get the subtotal

gross profit. This amount is the profit left after “paying for” the merchandise that was sold to the

customer. It must be used to “pay” the retailer’s operating expenses, such as salaries, rent, utilities, and

advertising. It might be beneficial to clarify up front that a merchandising business both buys and sells

merchandise inventory. Make sure the student can put on the buyer’s hat and the seller’s hat and

distinguish between the two activities.

Chapter 6 Accounting for Merchandising Businesses 6-5

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Objective 1 also introduces Merchandise Inventory, explaining that this account is reported as a current

asset on the balance sheet.

OBJECTIVE 2

Describe and illustrate the accounting for merchandise transactions.

SYNOPSIS

NetSolutions becomes a retailer in this chapter, and its transactions are illustrated by using a simplified

general journal. Using a perpetual inventory system, the merchandise available for sale and the cost of

goods sold are continuously updated. As computerized inventory is widely used, this method has become

more common. When merchandise is purchased by the retailer, an inventory account is debited and the

credit goes to either Cash or Accounts Payable. The terms laying out how the merchandise is to be paid

for are called credit terms. If payment on delivery is required, the terms are cash or net cash. If the buyer

is permitted an amount of time to pay, it is called the credit period. The credit period usually begins with

the date of the invoice. Terms expressed as 2/10, n/30 mean a discount of 2 percent will be given if the

invoice is paid within 10 days and the net amount is due within 30 days. Exhibit 3 shows a typical invoice

with credit due terms, and Exhibit 4 illustrates how to count days for the credit terms. Discounts taken by

the buyer are called purchase discounts. Under the perpetual inventory system, the buyer debits

Merchandise Inventory and credits Accounts Payable assuming all purchase discounts are taken. In this

way, merchandise inventory shows the net amount paid to the buyer.

If a retailer returns any merchandise, the retailer may request an allowance for merchandise returned.

From the buyer’s perspective, these returns are called purchases returns and allowances. The buyer sends

the seller a debit memo, which shows the seller the amount the buyer is requesting to debit to Accounts

Payable and also the reasons for the request. The buyer then debits Accounts Payable and credits

Merchandise Inventory. If the buyer is granted the allowance prior to paying the invoice, the amount is

deducted before computing any discounts.

Cash sales are recorded as a debit to Cash and a credit to Sales for the amount of the sale. Using the

perpetual inventory system, the decrease in inventory must also be recorded at the same time. Cost of

Goods Sold is debited, and Inventory is credited for the amount the inventory cost the buyer. If a credit

card is used, the transaction is recorded as a cash sale and the credit card processing fee charged the

retailer is paid periodically by the retailer. Credit card companies charge retailers a processing fee, which

when paid is recorded as a debit to an expense account and a credit to Cash. If the retailer sells on

account, Accounts Receivable is debited, Sales is credited, and the cost of merchandise sold and

merchandise inventory are recorded as above. If the seller is offering the buyer credit terms, it will reduce

the amount of sales. If the product is returned, it will also reduce the amount of sales.

Purchases and sales of merchandise often involve freight costs. FOB (free on board) shipping point means

that ownership of the merchandise passes to the buyer when it is picked up by the freight carrier. This also

means that the buyer will be paying the shipping costs. FOB destination means ownership of the

merchandise does not pass to the buyer until it is physically received. This means that shipping costs are

usually paid by the seller. In the first case, shipping costs are paid by the buyer and debited directly to the

inventory account. When freight costs are paid by the seller, the cost of the freight is debited to an

expense account. These freight terms are summarized in Exhibit 8. Exhibit 9 summarizes how these

transactions are journalized using T accounts.

6-6 Chapter 6 Accounting for Merchandising Businesses

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Another topic that is addressed in the chapter is sales tax. When a retailer sells merchandise to the end

consumer, a liability for sales tax is incurred. The seller collects the taxes at the time of sale. Accounts

Receivable is debited for the total amount, Sales is credited for only the price of the merchandise, and an

additional amount is credited to the sales tax payable account. Businesses that sell to other businesses for

resale do not charge sales taxes. These businesses may offer trade discounts to other businesses that are

not offered to consumers. Usually, only the net price is recorded in this type of transaction.

Key Terms and Definitions

Cash Refund - An amount paid by the seller to the buyer for merchandise that is defective, is

damaged during shipment, or does not meet the buyer’s expectations.

Credit Memorandum (Credit Memo) - A form used by a seller to inform the buyer of the

amount the seller proposes to credit to the account receivable due from the buyer.

Credit Period -The amount of time the buyer is allowed in which to pay the seller.

Credit Terms - Terms for payment on account by the buyer to the seller.

Customer Allowance - Returns to the seller by the customer or reductions from the initial selling

price due to defective or damaged merchandise or goods that did not meet the customer’s

expectations.

Customer Discounts - A variety of discounts offered by the seller as incentive for the customer

to act in a way benefiting the seller.

Customer Refunds Payable - A liability account for estimated refunds and allowances that will

be paid or granted customers in the future.

Debit Memorandum (Debit Memo) - A form used by a buyer to inform the seller of the amount

the buyer proposes to debit to the account payable due the seller.

Estimated Returns Inventory - A current asset that is reported on the balance sheet after

inventory.

FOB (Free on Board) Destination - Freight terms in which the seller pays the transportation

costs from the shipping point to the final destination.

FOB (Free on Board) Shipping Point - Freight terms in which the buyer pays the transportation

costs from the shipping point to the final destination.

Invoice - The bill that the seller sends to the buyer.

Periodic Inventory System - The inventory system in which the inventory records do not show

the amount available for sale or sold during the period.

Perpetual Inventory System - The inventory system in which each purchase and sale of

merchandise is recorded in an inventory account.

Physical Inventory - A detailed listing of merchandise on hand.

Purchases Discounts - Discounts taken by the buyer for early payment of an invoice.

Purchases Returns and Allowances - From the buyer’s perspective, returned merchandise or an

adjustment for defective merchandise.

Sales Discounts - From the seller’s perspective, discounts that a seller may offer the buyer for

early payment.

Trade Discounts - Discounts from the list prices in published catalogs or special discounts

offered to certain classes of buyers.

Wholesalers - Companies that sell merchandise to other businesses rather than to the public.

Chapter 6 Accounting for Merchandising Businesses 6-7

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Relevant Example Exercises and Exhibits

Exhibit 2 – Chart of Accounts for NetSolutions as a Merchandising Business

Exhibit 3 – Invoice

Exhibit 4 – Credit Terms

Exhibit 5 – Debit Memo

Example Exercise 6-2 – Purchases Transactions

Exhibit 6 – Credit Memo

Exhibit 7 – Journal Entries to Record Customer Refunds, Allowances, and Returns

Example Exercise 6-3 – Sales Transactions

Exhibit 8 – Freight Terms

Example Exercise 6-4 – Freight Terms

Exhibit 9 – Recording Merchandise Inventory Transactions

Exhibit 10 – Illustration of Merchandise Inventory Transactions for Seller and Buyer

Example Exercise 6-5 – Transactions for Buyer and Seller

SUGGESTED APPROACH

This objective demonstrates to the student that merchandising businesses engage in purchasing and

selling of merchandise inventory. First, the purchase of inventory is demonstrated using the perpetual

method of accounting for inventory. Note that the periodic method is demonstrated in the appendix to the

chapter.

The second part of this objective covers the entries to record sales in a perpetual inventory system. Begin

by stressing that selling merchandise to a customer requires two entries—one to record the sales revenue

and another to remove the item sold from merchandise inventory.

DEMONSTRATION PROBLEM—Entries for Merchandise Purchases

Purchases of merchandise for resale to a customer are recorded in the merchandise inventory account.

Point out that this account is an asset. Therefore, it is debited whenever inventory is increased and

credited whenever inventory is decreased.

Handout 6-1 lists purchase-related transactions for S & V Office Supply Company. Read the first

transaction to your students and ask them to journalize it in their notes. After giving them a minute to

work, show them the correct journal entry. Proceed with the other transactions listed on the handout. The

correct journal entries are listed on Handout 6-2. Use transaction 5 to explain the concept of a debit memo

in regard to returned merchandise.

The transactions on Handout 6-1 do include references to credit terms (e.g., 2/10, n/30). Remind students

that all merchandise purchases are recorded at the net purchase price; the buyer debits Merchandise

Inventory for the amount of the invoice less the discount, if a discount is offered.

6-8 Chapter 6 Accounting for Merchandising Businesses

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

DEMONSTRATION PROBLEM—Entries to Record Merchandise Sales

Handout 6-3 presents a matrix that explains the new accounts related to sales. Review these accounts with

your class.

Handout 6-4 lists several sales-related transactions for S & V Office Supply Company. One method to

present this material is to give the students examples of the entries to record the sale of inventory items in

lecture format. Another is to allow students to decipher the entries on their own. Try reading the first

transaction to your students and ask them to journalize it in their notes. After giving them a minute to

work, show them the correct journal entry. Proceed with the other transactions listed on the handout. The

correct journal entries are listed on Handouts 6-5 and 6-6. Use transaction 4 to demonstrate the use of a

credit memo for acknowledgement of returned merchandise.

WRITING EXERCISE—Recording Merchandise Sales

To emphasize some of the operational considerations in recording sales, ask your students to write

answers to one or more of the following questions.

1. Why would a retailer offer customers a discount for timely payment?

2. If you owned a merchandising business, how would you decide which credit cards, if any, to accept?

3. Which of the following credit terms would be more generous to your customers: n/30 or n/eom?

Possible responses: (1) Retailers offer discounts to customers to encourage them to pay early to improve

cash flow. (2) A large expense for merchandisers is credit card fees. These costs would come into the

decision-making process. On the other hand, the convenience of consumers using credit cards and those

cards that the majority of buyers carry will also factor into this decision process. (3) The only time that

n/eom is more favorable is when an invoice is issued on the first day of the month in a month that has 31

days.

LECTURE AID—Discounts

For many students, a 2 percent discount doesn’t sound very impressive. They may need a little help

understanding the true financial impact of taking discounts on purchases. The following questions will

stress the savings of taking discounts:

1. What is the net savings from borrowing at a 12 percent interest rate in order to take the discount on a

$10,000 purchase, terms 1/10, n/30? Answer: $34 [$100 – ($9,900 20/360 12%)].

2. What is the interest rate earned on taking a discount with terms 3/15, n/60? Answer: 24 percent (3%

360/45).

Chapter 6 Accounting for Merchandising Businesses 6-9

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

LECTURE AID—Transportation Costs on Sales

If merchandise is sold FOB destination, the seller is responsible for paying the shipping cost. The cost is

debited to Freight Out or Delivery Expense. For example, assume goods costing $100 are sold to a

customer on account for $250, terms FOB destination. The freight cost paid to have these goods delivered

is $25. The following entries are needed to record this sale and the transportation costs:

Accounts Receivable………… 250

Sales…………………. 250

Cost of Merchandise Sold…… 100

Merchandise Inventory 100

Delivery Expense………….. 25

Cash…………………. 25

FOB (free on board) terms identify (1) when legal title to goods passes from seller to buyer and (2) who is

responsible for paying transportation costs. Handout 6-7 lists the operational implications of FOB terms.

Notice that Handout 6-7 points out that the buyer bears the risk of loss during transportation when

merchandise is shipped FOB shipping point. Therefore, the buyer should make sure that the merchandise

is insured against loss during shipment.

A couple of points related to shipping terms usually need special emphasis. First, when merchandise is

shipped FOB shipping point, the seller frequently prepays the transportation costs and adds this amount to

the buyer’s invoice. Second, remind students that transportation costs are not eligible for early payment

discounts. Those discounts apply only to the cost of the merchandise purchased. To test their

understanding of these concepts, ask them to compute the cash to be paid in the following problem.

Logan Appliances purchased $8,000 of merchandise, 2/10, n/30, FOB shipping point. The seller prepaid

the shipping charges of $200. If Logan pays for this merchandise within the discount period, how much

should Logan remit to the seller? (Answer: $8,040)

DEMONSTRATION PROBLEM—Transportation Costs on Purchases

Ask your students to record the transactions related to the purchase of merchandise and transportation

costs on Handout 6-8. The correct entries are listed on Handout 6-9.

TEACHING SUGGESTION—Chart of Accounts, Trade Discounts, and Sales

Tax

Chart of Accounts: After explaining the text’s system, it is interesting to point out the variety in charts of

accounts and their numbering systems by providing some real-world examples. Ask students to bring in

copies of charts of accounts for merchandising businesses. Students may have access to charts of accounts

through their job or the job of a relative. There are also several websites that provide sample charts of

accounts to various industries. These can be found by searching for “chart of accounts” using an Internet

6-10 Chapter 6 Accounting for Merchandising Businesses

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

search engine. Many industry trade organizations will provide these samples on their website. As an

alternative, you may want to describe the chart of accounts for a local company with which you are

familiar.

In discussing the chart of accounts for a merchandising firm, the text uses a three-digit account number.

This reflects the growing number of accounts required by the increased complexity of a merchandiser’s

accounting transactions.

Under the three-digit chart of accounts, the first digit represents the account classification (1 for assets, 2

for liabilities, etc.). The second digit represents the subclassification (11 for current assets and 21 for

current liabilities). The third digit identifies the specific account.

Trade Discounts: To introduce trade discounts to your students, you need only to define the term and

give a quick example. A trade discount is a discount off the normal (or list) price of merchandise given to

a certain class of buyers, such as customers buying wholesale, not-for-profits, or governmental agencies,

etc. If merchandise with a list price of $700 is sold to a customer entitled to a 25 percent trade discount,

the selling price is reduced to $525 ($700 25% = $175; $700 – $175 = $525). Remind students that

trade discounts are not shown separately in journal entries. The amount credited to Sales (and debited to

Cash or Accounts Receivable) is simply the discounted price.

Sales Tax: Unless your students have lived exclusively in a state that does not charge sales tax, they will

already be familiar with this concept. Remind students that when sales tax is collected by a merchandiser

at the time of a sale, it is recorded in a liability account (Sales Tax Payable); the merchandiser is obligated

to remit the sales tax collected to the appropriate government authority. You may want to refer to the

journal entries related to sales tax in the text.

OBJECTIVE 3

Describe and illustrate the adjusting process for a merchandising business.

SYNOPSIS

Using the perpetual inventory system, the inventory account is constantly updated. This means the

amount in the inventory account should be equal to the amount of merchandise available for sale at any

point in time. However, retailers often experience loss from shoplifting, employee theft, or errors, and this

causes discrepancies between the inventory account and the merchandise actually available for sale. The

physical inventory on hand at the end of the accounting period in usually less than shown in the inventory

account. This difference is called inventory shrinkage or shortage. This shrinkage is recorded by an

adjusting entry: Cost of Merchandise Sold is debited and Merchandise Inventory is credited. After the

adjusting entry is recorded, the merchandise inventory account should reflect the physical inventory

count. If this amount becomes too large, a business may decide to record this in a separate account called

Merchandise Inventory Shrinkage.

Chapter 6 Accounting for Merchandising Businesses 6-11

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Two adjusting entries are necessary for estimated allowances and returns. The first adjusting entry debits

Sales and credits Customer Refunds Payable. The second entry debits Estimated Returns Inventory and

credits Cost of Merchandise Sold.

Key Term and Definition

Inventory Shrinkage (Inventory Shortage) - The amount by which the merchandise for sale, as

indicated by the balance of the merchandise inventory account, is larger than the total amount of

merchandise counted during the physical inventory.

Relevant Example Exercises

Example Exercise 6-6 – Inventory Shrinkage

Example Exercise 6-7 – Customer Allowances and Returns

SUGGESTED APPROACH

This objective introduces the adjusting entry for inventory shrinkage. Remind students that merchandisers

also record any of the adjusting entries introduced in Chapter 3 that are applicable (e.g., supplies used,

insurance expired, wages owed to employees, fees earned, etc.). It also discusses closing entries; point out

to students that closing entries for a merchandising business are similar to those for a service business.

Discuss the new merchandising accounts that are added as part of the closing process. Cost of

merchandise sold is an all new merchandising account that gets closed along with the already familiar

expense accounts. The revenue account for a merchandising business is the sales account and requires a

debit entry to close the account.

The adjusting process may require Merchandise Inventory to be adjusted for various causes (see text).

Ask students to name a few. Large shortages can exist due to spoilage and shrinkage or maybe theft

(employee, customer, unknown). The related expenses are Cost of Merchandise Sold, and likewise,

Merchandise Inventory has disappeared, so it must be reduced (credited). Large shrinkage/shortages may

be put in a separate expense account, but they still increase Cost of Merchandise Sold. Physical inventory

and book inventory must agree at the end of the period.

LECTURE AID—Adjusting Entry for Inventory Shrinkage

Unfortunately, inventory shrinkage is considered a normal cost of operations for a retailer. Theft of

inventory (shoplifting), damaged inventory, and mistakes in recording inventory can never be totally

eliminated. Therefore, the inventory account must be adjusted prior to preparing financial statements. Any

shrinkage is recorded as an expense.

For example, assume a company’s perpetual inventory records show that there should be $89,500 of

inventory on hand. (Emphasize that the perpetual records show what should be in inventory based on

merchandise purchased and sold during the year.) However, a physical inventory count reveals that only

$87,000 is actually on hand at year-end. Ask your students to determine the amount of shrinkage.

(Answer: $2,500)

6-12 Chapter 6 Accounting for Merchandising Businesses

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

This shrinkage is recorded as follows:

Cost of Merchandise Sold……….. 2,500

Merchandise Inventory….. 2,500

You may want to point out that if the amount of shrinkage is unusually large, it is better to record it in a

separate account, such as Loss from Merchandise Inventory Shrinkage; stress that all companies must do

a physical inventory count at least once per year to verify the information in the perpetual inventory

records.

LECTURE AID—Adjusting Entries for Customer Refunds, Allowances, and

Returns

The amounts reported on the financial statements must accurately reflect the position of the company.

Sellers usually experience customer returns and/or grant allowances as part of doing business. Therefore,

the financial statements should reflect the anticipation of these returns and allowances.

Companies are required to estimate returns and allowances at the end of the accounting period and

prepare two adjusting entries. The first entry decreases sales to the amount of sales that the company

actually expects to earn. It also creates a liability account to estimate the amount that will be paid to

customers. The second entry reduces Cost of Merchandise Sold for the amount of inventory expected to

be returned. Since the inventory is still in the hands of the customer, the inventory account cannot be

increased. Instead, the estimated cost of inventory to be returned is recorded in Estimated Returns

Inventory. The adjusting entries are recorded as follows. Assume the estimated amount of returns is

$1,500 and the cost of inventory related to those returns is $900.

Sales……..……..……..……..………... 1,500

Customer Refunds Payable….. 1,500

Estimated Returns Inventory…………. 900

Cost of Merchandise Sold …… 900

In Objective 2, we saw the journal entries required when a customer returns merchandise. You may want

to review those at this time. Journal entry 4 on Handout 6-6 shows the following:

S & V Office Supply Company accepted a return of $50 worth of merchandise from a cash customer. The

cost of the merchandise returned was $30. The customer received a cash refund.

Customer Refunds Payable…..………. 50

Cash………………………….. 50

Merchandise Inventory …..…………. 30

Cost of Merchandise Sold ....... 30

Remind the students that if S & V allowed the customer to keep the inventory, only the first entry is

required.

Chapter 6 Accounting for Merchandising Businesses 6-13

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

OBJECTIVE 4

Describe and illustrate the financial statements of a merchandising business.

SYNOPSIS

Merchandising businesses have a few unique items in their financial statements. First, let’s take a look at

the multiple-step income statement shown in Exhibit 11. The first section shows sales. The cost of

merchandise sold is subtracted from sales to calculate gross profit. The Operating expenses section is

divided in two parts: selling expenses and administrative expenses. The total expenses are subtracted from

gross profit to calculate income from operations, and then there is a small section for other revenue and

expense before arriving at net income. Exhibit 12 displays the same information in a single-step income

statement. The statement of owner’s equity for a merchandising business does not differ from the service

business statement shown in previous chapters. The balance sheet may be presented two ways. In the

account form, the Assets section is displayed on the left side, and the liabilities and owner’s equity are on

the right. The balance sheet may also be presented in a downward sequence of three sections known as

the report form. The balance sheet for NetSolutions in report form is shown in Exhibit 14.

Closing entries are similar to a service business. Debit each revenue account for its balance, credit each

expense account for its balance, and credit owner’s capital account for net income. Debit the owner’s

capital account for a net loss. Cost of merchandise sold is a temporary account and is closed like an

expense account. Debit the owner’s capital account for the balance of the drawing account and credit the

drawing account. After the closing entries and post-closing trial balance are prepared, only permanent

accounts are shown on the post-closing trial balance.

Key Terms and Definitions

Administrative Expenses (General Expenses) - Expenses incurred in the administration or

general operations of the business.

Income from Operations (Operating Income) - Revenues less operating expenses and service

department charges for a profit or an investment center.

Multiple-Step Income Statement - A form of income statement that contains several sections,

subsections, and subtotals.

Other Expense - Expenses that cannot be traced directly to operations.

Other Revenue - Revenue from sources other than the primary operating activity of a business.

Selling Expenses - Expenses that are incurred directly in the selling of merchandise.

Single-Step Income Statement - A form of income statement in which the total of all expenses is

deducted from the total of all revenues.

Relevant Exhibits

Exhibit 11 – Multiple-Step Income Statement

Exhibit 12 – Single-Step Income Statement

Exhibit 13 – Statement of Owner’s Equity for Merchandising Business

Exhibit 14 – Balance Sheet for Merchandising Business

6-14 Chapter 6 Accounting for Merchandising Businesses

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

SUGGESTED APPROACH

This objective introduces the multiple-step income statement. This income statement format contains

various sections, subsections, and subtotals, which increase the length and complexity of the income

statement. Point out that the benefit of this more detailed format is greater flexibility in analyzing a

company’s performance. For example, the gross profit percentage (gross profit divided by sales) is used

to analyze the markup above cost charged by retailers.

The trap that many students fall into is blindly attempting to memorize the multiple-step income

statement line by line. Instead, they need to approach it as a series of pieces (sections) that must be fit

together to provide a total picture of a company—similar to fitting together pieces of a jigsaw puzzle.

Note: The format of the multiple-step income statement is significantly different in the area of Cost of

Merchandise Sold when periodic inventory is used than when perpetual inventory is used.

GROUP LEARNING ACTIVITY—Multiple-Step Income Statement

Before digging into the multiple-step income statement, you will need to define the new terms for your

students.

Sales: The total amount charged customers for merchandise sold. (This is a revenue account.)

Cost of Merchandise Sold: The cost to purchase the inventory being sold.

Gross Profit: Proceeds available for selling and administrative expenses.

Selling Expenses: Costs directly incurred in selling the merchandise, such as the cost of advertising or

commissions paid to salespersons.

Administrative Expenses: Costs incurred in the administration or general operations of the business, such

as the cost of office supplies or the salary paid to an accountant.

Income from Operations: Profit earned by the conducting company’s primary business of buying and

selling merchandise.

Other Revenue: Revenue from sources other than the company’s primary business, such as interest

revenue on a checking account or rent revenue from leasing unused space.

Other Expense: Costs incurred from activities other than the company’s primary business of buying and

selling its product, such as interest expense on business loans.

You may want to demonstrate how intuitive the calculations are on the income statement by asking the

following question:

Assume a retailer sold $100 in merchandise to a customer on account. That customer returned $10 of the

merchandise. The customer also paid for the remaining merchandise early, entitling her to a $5 discount.

What amount of revenue was really earned on the sale? (Answer: $85)

Handout 6-10 shows the individual sections of the multiple-step income statement and how they

interrelate. Review this handout with the class, explaining each section and its placement in the statement.

Handout 6-11 shows an adjusted trial balance for Gem City Music. Divide students into small groups and

ask them to prepare an income statement for this retailer. A completed income statement is shown on

Handout 6-12.

Chapter 6 Accounting for Merchandising Businesses 6-15

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

GROUP LEARNING ACTIVITY—Statement of Owner’s Equity and Balance

Sheet

Point out that there are no differences between the statements of owner’s equity for a service business and

a merchandiser. Remind students that the only difference on the balance sheet is that a merchandising

company will show Merchandise Inventory and Estimated Returns Inventory as current assets and

Customer Refunds Payable as a current liability on its balance sheet. If time permits, your students can

review these financial statements by preparing a statement of owner’s equity and balance sheet from the

adjusted trial balance for Gem City Music on Handout 6-11. See Handouts 6-13 and 6-14 for the

completed financial statements.

LECTURE AID—Closing Process for Merchandising Business

The process of closing entries has not changed from Chapter 4; there are simply more accounts to close.

In a perpetual inventory system, the cost of merchandise sold account is closed to the owner’s capital

account, along with the other debit balance accounts shown in the Income Statement column of the end-

of-period spreadsheet (work sheet). The sales account is the revenue account which is also closed to the

owner’s capital account.

OBJECTIVE 5

Describe and illustrate the use of asset turnover in evaluating a company’s operating

performance.

SYNOPSIS

To measure how effectively a company uses its assets to generate sales, the asset turnover (Sales/Average

Total Assets) is computed. This objective gives an example of asset turnover and shows the calculation

for average assets to be the average of the assets at the beginning and end of the year.

Key Term and Definition

Asset Turnover - A measure of how effectively a business is using its assets to generate sales.

Relevant Example Exercise

Example Exercise 6-8 – Asset Turnover

6-16 Chapter 6 Accounting for Merchandising Businesses

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

SUGGESTED APPROACH

Explain to students that the assets of a company are “used up” as a normal part of conducting business.

How efficiently a company uses those assets to generate sales is another good indicator of the company’s

operating performance. As the text indicates, the value of the assets used to compute the asset turnover

may be the total assets at the end of the year, the average between the beginning and the end of the year,

or the average of the monthly assets.

APPENDIX—The Periodic Inventory System

SYNOPSIS

The periodic inventory system may be used for businesses that use a manual accounting system. In the

periodic system, the cost of merchandise sold is determined at the end of the period. An example is shown

in Exhibit 17. Additional accounts used in this system are shown in the chart of accounts in Exhibit 15.

Using the periodic system, instead of recording merchandise purchases in the inventory account,

purchases, purchases discounts, purchase returns and allowances, and freight in accounts are used. The

adjusting process is the same under this system with the exception of the adjustment for shrinkage. Since

the inventory account is not kept up to date, shrinkage can be determined only indirectly in the cost of

merchandise sold. The closing process is the same under the periodic system except that the names of the

accounts change. Examples of the closing entries are shown in Exhibit 18.

Relevant Exhibits

Exhibit 15 – Chart of Accounts Under the Periodic Inventory System

Exhibit 16 – Transactions Using the Periodic Inventory System

Exhibit 17 – Determining Cost of Merchandise Sold Using Periodic Inventory

Exhibit 18 – Closing Entries: Periodic Method

SUGGESTED APPROACH

Chapter 6 assumes that a merchandising business uses a perpetual inventory system. Some businesses

may still use a periodic inventory system, and this appendix points out the differences in the two systems.

Point out Exhibit 16 in the text, and emphasize the difference in accounts and timing of recording Cost of

Merchandise Sold between the periodic and perpetual inventory systems.

Problems 6-8A or 6-8B in the textbook can be used to demonstrate the entries and differences between

the two inventory methods.

LECTURE AID—Calculating Cost of Merchandise Sold Using the Periodic

Inventory System

This activity presents a brief comparison of the perpetual and periodic inventory systems. Handouts 6-15

through 6-17 contrast the two inventory systems, show the costs and benefits of a perpetual inventory

Chapter 6 Accounting for Merchandising Businesses 6-17

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

system, and offer insight on how businesses choose an inventory system. To illustrate the essence of a

perpetual inventory system, relate it to a checkbook. Maintaining a checkbook register for a bank account

is a type of perpetual inventory system. By tracking increases (deposits) and decreases (withdrawals or

checks written) in the checkbook register, you can keep a running balance of your cash.

A merchandiser that uses the periodic inventory system must compute cost of merchandise sold when

preparing an income statement. This calculation is based on the amount of inventory purchased and the

amount in inventory at the beginning and end of the period. The following story will illustrate this

calculation.

Assume that you are a “Twinkies junkie.” Whenever you study, you eat Twinkies. One evening, before a

big accounting test, you go to your cupboard and find that you have only three Twinkies left. You know

that three Twinkies will never get you through the night, so you head off to the grocery to buy another

box. The box contains 12 Twinkies. You then proceed to study and eat, study and eat, and study and eat.

The next morning, you decide to figure out how many Twinkies you ate while studying. You didn’t count

the Twinkies as you ate them, but you know the old box is empty and the new box has only five Twinkies

left. How many Twinkies did you eat? (After waiting for a response, continue the illustration.)

Let’s review your calculation using accounting terminology. You started with a beginning inventory of

three Twinkies. You then purchased 12 Twinkies. This gave you 15 Twinkies available for consumption.

Since five Twinkies were left in ending inventory, you must have eaten 10.

This is essentially the calculation of cost of merchandise sold under a periodic inventory system:

Merchandise Inventory on hand at the beginning of the year

+ Cost of Merchandise Purchased

Merchandise Available for Sale

– Merchandise Inventory left at the end of the year

Cost of Merchandise Sold

When purchasing merchandise inventory, a business may be required to pay transportation costs to have

the merchandise delivered from the supplier. The purchaser may also receive early payment discounts or

make returns of unwanted merchandise. Therefore, the cost of merchandise purchased must be calculated

as follows:

Purchases

– Purchase Returns and Allowances

– Purchase Discounts

Net Purchases

+ Transportation In

Cost of Merchandise Purchased

Handout 6-18 shows these calculations and how they fit together.

Handout 6-19 provides a practice problem related to the calculation of cost of merchandise sold in the

periodic system. Ask your students to calculate the cost of merchandise purchased (answer: $975) and the

cost of merchandise sold (answer: $905).

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-1

PURCHASE TRANSACTIONS FOR S & V OFFICE

SUPPLY COMPANY

1. S & V purchased $500 worth of merchandise for cash.

2. S & V purchased $4,000 of merchandise on account; terms n/30.

3. S & V paid for the merchandise purchased in transaction 2.

4. S & V purchased $2,000 of merchandise from its supplier on account;

terms 3/15, n/45.

5. S & V returned $100 worth of the merchandise purchased in

transaction 4 because it was damaged.

6. S & V paid for the merchandise purchased in transaction 4, less the

amount returned in transaction 5. This invoice was paid within the

discount period.

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-2

PURCHASE TRANSACTIONS FOR S & V OFFICE

SUPPLY COMPANY

(Solution)

1. S & V purchased $500 worth of merchandise for cash.

Merchandise Inventory ........................................... 500

Cash .................................................................... 500

2. S & V purchased $4,000 of merchandise on account; terms n/30.

Merchandise Inventory ........................................... 4,000

Accounts Payable ............................................... 4,000

3. S & V paid for the merchandise purchased in transaction 2.

Accounts Payable .................................................... 4,000

Cash .................................................................... 4,000

4. S & V purchased $2,000 of merchandise from its supplier on account;

terms 3/15, n/45.

Merchandise Inventory ........................................... 1,940

Accounts Payable ............................................... 1,940

5. S & V returned $100 worth of the merchandise purchased in

transaction 4 because it was damaged.

Accounts Payable .................................................... 97

Merchandise Inventory ....................................... 97

6. S & V paid for the merchandise purchased in transaction 4, less the

amount returned in transaction 5. This invoice was paid within the

discount period.

Accounts Payable .................................................... 1,843

Cash .................................................................... 1,843

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-3

MERCHANDISE SALES

The following are used to record sales of merchandise to customers:

Account

Classifi- Normal

Account Purpose cation Balance

Sales Used to record Revenue Credit

sales revenue when-

ever a sale is made

to a cash or credit

customer.

Cost of Used to record the cost Expense Debit

Merchandise of inventory items sold to

Sold customers. The inventory

items sold must be removed

from the merchandise

inventory account.

Credit Card Used to record the service Expense Debit

Expense fee charged by credit card

companies.

Sales Tax Used to record sales tax Liability Credit

Payable collected by the seller;

these taxes must be paid

to the appropriate tax

authority (e.g.,

state or county).

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-4

SALES TRANSACTIONS FOR S & V OFFICE

SUPPLY COMPANY

1. Sold $500 in merchandise to a cash customer. The cost of the

merchandise sold was $280.

2. Sold $1,200 worth of merchandise to a customer who charged the

merchandise to her VISA card. The cost of the merchandise sold was

$950. [Hint: Bank card sales (VISA and MasterCard) are treated the

same as cash sales because the retailer may deposit the credit card

slips directly into his or her bank account.]

3. Sold $2,000 in merchandise to a credit customer on a store account.

The terms of the sale are 2/10, n/30. The cost of the merchandise sold

was $1,600.

4. Accepted a return of $50 worth of merchandise from the cash

customer in transaction 1. The cost of the merchandise returned was

$30. The customer received a cash refund.

5. Received payment from the credit customer in transaction 3 within

the discount period.

6. Paid the service fee on VISA and MasterCard sales to Third National

Bank, $75.

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-5

SALES TRANSACTIONS FOR S & V OFFICE

SUPPLY COMPANY

(Solution)

1. Sold $500 in merchandise to a cash customer. The cost of the

merchandise sold was $280.

Cash ......................................................................... 500

Sales .................................................................... 500

Cost of Merchandise Sold ....................................... 280

Merchandise Inventory ....................................... 280

2. Sold $1,200 worth of merchandise to a customer who charged the

merchandise to her VISA card. The cost of the merchandise sold was

$950.

Cash ......................................................................... 1,200

Sales .................................................................... 1,200

Cost of Merchandise Sold ....................................... 950

Merchandise Inventory ....................................... 950

3. Sold $2,000 in merchandise to a credit customer on a store account.

The terms of the sale are 2/10, n/30. The cost of the merchandise sold

was $1,600.

Accounts Receivable ............................................... 1,960

Sales .................................................................... 1,960

Cost of Merchandise Sold ....................................... 1,600

Merchandise Inventory ....................................... 1,600

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-6

SALES TRANSACTIONS FOR S & V OFFICE

SUPPLY COMPANY

Solution (Concluded)

4. Accepted a return of $50 worth of merchandise from the cash

customer in transaction 1. The cost of the merchandise returned was

$30. The customer received a cash refund.

Customer Refunds Payable ..................................... 50

Cash .................................................................... 50

Merchandise Inventory ........................................... 30

Cost of Merchandise Sold .................................. 30

5. Received payment from the credit customer in transaction 3 within

the discount period.

Cash ......................................................................... 1,960

Accounts Receivable .......................................... 1,960

6. Paid the service fee on VISA and MasterCard sales to Third National

Bank, $75.

Credit Card Expense ............................................... 75

Cash .................................................................... 75

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-7

FREIGHT TERMS

FOB FOB

Shipping Point Destination

Ownership (title)

passes to buyer

when merchandise Delivered to Received

is .......................................... freight carrier by buyer

Transportation

costs are paid

by ........................................ Buyer Seller

Risk of loss during

transportation

belongs to ............................ Buyer Seller

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-8

PURCHASE TRANSACTIONS FOR S & V OFFICE

SUPPLY COMPANY—FREIGHT TERMS

1. S & V purchased $1,000 worth of merchandise on account; terms

2/10, n/30, FOB shipping point. The freight costs of $50 were prepaid

by the seller and added to the invoice.

2. S & V paid for the merchandise purchased in transaction 1 within the

discount period. (Hint: The discount does not apply to the

transportation costs.)

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-9

PURCHASE TRANSACTIONS FOR S & V OFFICE SUPPLY

COMPANY—FREIGHT TERMS

(Solution)

1. S & V purchased $1,000 worth of merchandise on account; terms

2/10, n/30, FOB shipping point. The freight costs of $50 were prepaid

by the seller and added to the invoice.

Merchandise Inventory ....................................... 1,030

Accounts Payable ........................................... 1,030

2. S & V paid for the merchandise purchased in transaction 1 within the

discount period.

Accounts Payable ................................................ 1,030

Cash ................................................................ 1,030

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

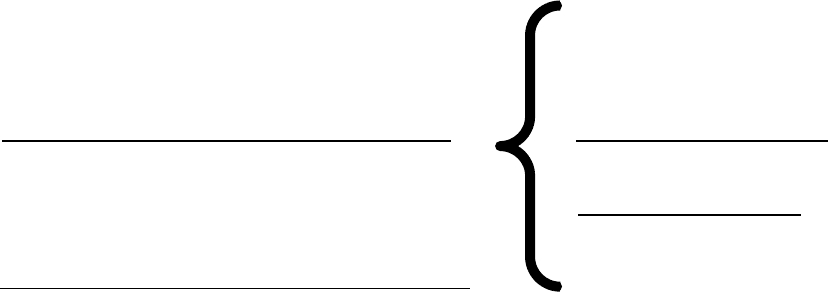

Handout 6-10

THE INCOME STATEMENT—AN EXPANDED VIEW

Single-Step Multiple-Step

Income Income

Statement Statement

(Chapters 1–4) (Chapter 6)

Revenues Revenue from Sales

– Expenses – Cost of Merchandise Sold

Gross Profit

Operating Expenses:

Selling Expenses

– Operating Expenses + Administrative Expenses

Total Operating Expenses

Income from Operations

+ Other Revenue

(i.e., Interest, Rent)

– Other Expenses

(i.e., Interest)

Net Income Net Income

{

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-11

ADJUSTED TRIAL BALANCE

Gem City Music

Adjusted Trial Balance

December 31, 20Y1

Cash ............................................................... 11,000

Accounts Receivable ..................................... 15,800

Merchandise Inventory .................................. 9,000

Estimated Returns Inventory ......................... 600

Office Equipment .......................................... 23,000

Accumulated Depreciation—

Office Equipment ..................................... 9,200

Accounts Payable .......................................... 15,000

Customer Refunds Payable ........................... 1,000

Salaries Payable ............................................. 1,250

M. Marx, Capital ........................................... 11,500

M. Marx, Drawing ......................................... 12,800

Sales ............................................................... 187,100

Cost of Merchandise Sold ............................. 100,000

Rent Expense ................................................. 7,800

Sales Salaries Expense .................................. 17,700

Office Salaries Expense................................. 22,550

Depreciation Expense—

Office Equipment ..................................... 2,800

Interest Expense............................................. 2,000

Total ............................................................... 225,050 225,050

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-12

INCOME STATEMENT

Gem City Music

Income Statement

For the Year Ended December 31, 20Y1

Sales ................................................ $187,100

Cost of merchandise sold ................... 100,000

Gross profit ......................................... $ 87,100

Operating expenses:

Selling expenses:

Sales salaries expense ............. $17,700

Total selling expenses ........ $17,700

Administrative expenses:

Rent expense ........................... $ 7,800

Office salaries expense ........... 22,550

Depr. expense—office equip. . 2,800

Total administrative expenses 33,150

Total operating expenses ............. 50,850

Income from operations...................... $ 36,250

Other expense:

Interest expense ........................... 2,000

Net income ...................................... $ 34,250

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-13

STATEMENT OF OWNER’S EQUITY

Gem City Music

Statement of Owner’s Equity

For the Year Ended December 31, 20Y1

M. Marx, capital, January 1, 20Y1 ..................... $11,500

Net income for the year ...................................... $ 34,250

Withdrawals ........................................................ (12,800)

Increase in owner’s equity .................................. 21,450

M. Marx, capital, December 31, 20Y1 .............. $32,950

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-14

BALANCE SHEET

Gem City Music

Balance Sheet

December 31, 20Y1

Assets

Current assets:

Cash ........................................................... $11,000

Accounts receivable .................................. 15,800

Merchandise inventory ............................. 9,000

Estimated returns inventory ...................... 600

Total current assets ............................... $36,400

Property, plant, and equipment:

Office equipment ...................................... $23,000

Less accumulated depreciation ................. 9,200

Total property, plant, and equipment ... 13,800

Total assets .................................................... $50,200

Liabilities

Current liabilities:

Accounts payable ...................................... $15,000

Customer refunds payable ........................ 1,000

Salaries payable ........................................ 1,250

Total liabilities ...................................... $17,250

Owner’s Equity

M. Marx, capital ............................................ 32,950

Total liabilities and owner’s equity ............... $50,200

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-15

TWO INVENTORY SYSTEMS

PERPETUAL:

The merchandise inventory account is increased when inventory is

purchased.

The merchandise inventory account is decreased when inventory is

sold to a customer.

Therefore, the merchandise inventory account always (perpetually)

shows the amount of inventory on hand.

PERIODIC:

Purchases of inventory are recorded in a purchases account.

Inventory is not removed from the accounting records when it is sold.

Therefore, the amount of inventory on hand must be determined by

taking a physical inventory count.

SUMMARY:

The perpetual inventory system requires more accounting entries, but it

provides more up-to-date information for managing inventory.

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-16

COST-BENEFIT ANALYSIS

IMPLEMENTING A PERPETUAL INVENTORY SYSTEM

Benefits:

1. Accounting records always show the amount of inventory on hand.

This will assist in:

a. Determining when to reorder inventory.

b. Determining how much inventory to reorder.

c. Analyzing whether an item of inventory is a “hot seller” or “slow

mover.”

d. Making decisions on markdowns or special promotions.

2. A physical inventory count is necessary only at year-end. This count

validates the perpetual inventory records.

Costs:

1. Hiring extra accounting personnel or increased fees paid to an

accounting service as the result of a greater number of transactions

that must be recorded and processed.

OR

2. Purchasing optical scanners and computerized equipment to track

purchases and sales of inventory items.

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-17

CHOOSING AN INVENTORY SYSTEM

Size of Unit Cost of Probable

Retailer Inventory Items Choice Reason

Small Low Periodic Perpetual inventory systems

may be too costly for a small

retailer who sells many low-

priced inventory items.

Small High Perpetual Because the cost of inventory

items is high, a smaller

number of the items would

be sold during the year. This

keeps the cost of a perpetual

system affordable. In addition,

tight control over the

high-cost inventory items is

essential.

Large Low Perpetual A large retailer will have

sufficient sales volume to

cover the cost of a perpetual

system even if the cost of

inventory items is relatively

low. The sales volume and

number of inventory items

make it difficult to manage

the business without

inventory records that are

updated daily.

Large High Perpetual The sales volume and need

for tight inventory control of

high-priced items will dictate

the use of a perpetual

inventory system.

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-18

CALCULATING COST OF MERCHANDISE SOLD UNDER A

PERIODIC INVENTORY SYSTEM

Purchases

Merchandise Inventory, Beg. of Year – Purchase Returns and

Allowances

+ Cost of Merchandise Purchased – Purchase Discounts

Net Purchases

Merchandise Available for Sale + Transportation In

Cost of Merchandise

– Merchandise Inventory, End of Year Purchased

Cost of Merchandise Sold

© 2018 Cengage. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Handout 6-19

CALCULATING COST OF MERCHANDISE SOLD UNDER A

PERIODIC INVENTORY SYSTEM

Christopher’s Gourmet Chocolates is a small retail store that uses a

periodic inventory system. Compute Christopher’s cost of merchandise

sold for November based on the following information:

Inventory on November 1 ................ $ 280

Merchandise purchased .................... 1,000

Merchandise returned due

to quality problems .................... 50

Discounts on merchandise

purchased ................................... 20

Delivery costs for

merchandise purchased .............. 45

Inventory on November 30 .............. 350