search

2

Starbucks Benefits Plan Description

|

Reference Guide 4

Plan Highlights 5

Using the Plan 7

Future Roast 401(k) 9

Why Save in Future Roast 401(k)? 10

Eligibility 10

If you are rehired 11

Enrolling in Future Roast 401(k) 12

Beneficiary designations 12

Contributions to Your

Future Roast 401(k) Account 13

401(k) payroll contributions 13

Starbucks Match 14

Eligible pay 14

Exceeding IRS limits in a calendar year 14

Safe Harbor Plan qualification 15

Discrimination test annual limit 16

Tax credit for eligible savers 16

Rollover contributions 16

Starbucks discretionary

profit-sharing contributions 17

Investment Option Tiers 18

Target Date Retirement Investments

U.S. and Foreign Equity Investments

Bond and Stable Value Investments

ESG Sustainable Investments

The importance of diversifying the

investment of your accounts 19

The Future Roast 401(k)

default investment 20

For more information 20

Things to consider 20

Valuing your Future Roast 401(k)

account 20

Making your investment elections 21

Making changes to your

investment elections 21

Managing Your Account 22

Account statements 22

Frequent trading 23

Loans 23

Minimum and maximum loan amounts 24

Applying for a loan 24

Loan fees 25

Repaying your loan 25

More about loan defaults 27

Early loan payoff 27

Future Roast 401(k)

Savings Plan

main

contents

||

back

page

}

|

page

Future Roast 401(k)

Savings Plan

search

3

Starbucks Benefits Plan Description

|

Future Roast 401(k)

Savings Plan

Starbucks Benefit Plan Description

|

3

Withdrawals During Employment 28

Hardship withdrawals 28

HEART Act (active military) withdrawals 29

Qualified Birth or Adoption Distribution 29

Age 59½ withdrawals 29

Withdrawals from your rollover account 30

Total distribution from

Future Roast 401(k) 30

If you are disabled 30

Recontribution of a CARES Act

withdrawal 30

If You Terminate Employment with

Starbucks and Any Related Company 31

Termination withdrawals 31

Recontribution of a CARES Act

withdrawal after separation 32

Deferred payment 32

Rollover distributions into another plan 32

Pre-tax rollover to a Roth IRA 33

Two ways to roll over your

account balance 33

Requesting a rollover or withdrawal 34

Death benefit 34

Beneficiary designation 35

Administrative Information 35

Your rights and responsibilities 35

Paying income taxes 35

Contributions 36

Hardship withdrawals and taxes 37

Loans and taxes 37

Rollovers 37

Tax-exempt Thrift Savings Plan (TSP)

rollovers 37

Pre-tax rollover to a Roth IRA 37

General Provisions 38

Loss or denial of benefits 38

Rights of participants 38

Plan amendment or termination 38

PBGC coverage 38

Disclaimer 38

Assignments 39

Qualified domestic relations order 39

Responsibility for investment

decisions 39

How 401(k) contributions affect

other benefits 40

Tax treatment 40

Correction of errors 40

Top-heavy provisions 40

Your ERISA Rights 41

Your Rights Under USERRA 42

Plan Funding and Expenses 42

Claims 43

Claiming benefits 43

Procedures for benefit claims 43

Request for review 44

Limitations on legal action 44

Plan information for Starbucks

Corporation 401(k) Plan 45

STARBUCKS FINANCIAL WELL-BEING 46

What is Financial Well-being? 46

My Starbucks Savings 46

Starbucks Financial Resilience Toolkit 47

Starbucks Student Loan Management 48

Other Financial Well-Being Resources 49

search

main

contents

||

back

page

}

|

page

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

4

Starbucks Benefits Plan Description

|

search

REFERENCE GUIDE

Fidelity NetBenefits

SM

Log on to Fidelity NetBenefits (NetBenefits

SM

) via netbenefits.com

or call Fidelity to speak with a Service Representative for more

information about Future Roast 401(k), such as:

• Eligibility

• Enrollment

• Rollovers

• Account balance

• Investment options and fund prospectuses

• Investment changes

• Loans

• Changing beneficiaries

• Withdrawals and distributions

• Qualified domestic relations orders

Link to Fidelity NetBenefits

SM

via netbenefits.com

or mysbuxben.com

Virtually 24/7

For help with preparing Future Roast 401(k)

Qualified Domestic Relations Orders, link to

qdro.fidelity.com

Fidelity

(866) 697-1048 or (800) 587-5282 (Spanish line)

Representatives available weekdays

530 a.m. – 9 p.m. Pacific Time

Language translation and relay services available

Fidelity® Personalized Planning & Advice

Professional management of the investments in your

Future Roast 401(k) Plan account (optional fee-based service)

Log into netbenefits.com/plan for information on

the fee-based managed account advisory service available

through Fidelity.

(866) 811-6041

Fidelity representatives available weekdays

530 a.m. – 9 p.m. Pacific Time

Savings Team at Starbucks

Available to answer your specific questions about the

Future Roast 401(k) Plan

Starbucks Partner Contact Center

Call Starbucks Partner Contact Center for information about:

• Your paycheck

• Your payroll deductions

• Your payroll taxes

• Your change of address or other personal changes

Starbucks Coffee Company

P.O. Box 34067

Seattle, WA 98124-1067

(888) SBUX-411 or (888) 728-9411 weekdays

5 a.m. – 5 p.m. Pacific Time

Social Security Administration

Call the Social Security Administration or access its website to:

• Learn about Social Security benefits and how to apply

• Understand how Social Security works

• Request your free Personal Earnings and Benefit Estimate Statement

• Locate an office in your area

(800) 772-1213

socialsecurity.gov

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

5

Starbucks Benefits Plan Description

|

search

PLAN HIGHLIGHTS

Eligibility Partners on the Starbucks or a participating company’s U.S. payroll who:

• Are at least age 18 and

• Have completed 90 days of employment with Starbucks or any related company

Pre-tax 401(k)

contributions and/or Roth

after-tax contributions

You can choose to contribute from 1% to 75% of your eligible pay each pay period, in a combination of 401(k) pre-tax

and/or Roth after-tax contributions up to the annual IRS limit, $20,500 for calendar year 2022. For partners age 50 or

older in 2022, the IRS limit is $27,000.* Any Starbucks Match contributed to your account does not count toward these

dollar limitations. Your 401(k) pre-tax contributions and/or Roth after-tax contributions are deducted from your pay

and are credited to your account at Fidelity.

* The 2023 contribution limits have not been released by the IRS by the effective date of this document. When available, they will be communicated to

partners and posted on netbenefits.com.

Enrollment Partners will be able to enroll online or by phone starting approximately 75 days prior to attainment of eligibility.

Payroll contributions will start within one to two pay periods after the later of the date you enroll or the date you meet

the Plan’s eligibility requirements (90 days of employment, age 18 and on the Starbucks or a participating company’s

U.S. payroll).

Starbucks Match

(Safe Harbor Match)

Eligible partners who contribute to Future Roast 401(k) will receive matching contributions. As of January 1, 2022, and

for future calendar years (unless changed by Starbucks), the Starbucks Match is 100% of the first 5% of eligible pay*

contributed by eligible participants each pay period.

The Starbucks Match will be contributed along with your 401(k) pre-tax contributions and/or Roth after-tax

contributions each pay period. For any pay period in which you do not make 401(k) pre-tax contributions and/or Roth

after-tax contributions, you will not receive the Starbucks Match.

Eligible participants should consider contributing at least 5% of eligible pay* (in a combination of 401(k) pre-tax and/or

Roth after-tax contributions) each paycheck throughout the calendar year to maximize the Starbucks Match.

The Starbucks Match will be shown in your account as Safe Harbor Match contributions.

* The maximum amount of eligible pay that will be taken into consideration when calculating 401(k) pre-tax and or Roth after-tax contributions

and match for any calendar year is subject to IRS limits ($305,000 for calendar year 2022).

Vesting You are always 100% vested in all your accounts under the Plan, including 401(k) pre-tax, Roth after-tax, Match

(pre-2011), Starbucks Match, and any discretionary profit-sharing and rollover accounts.

Investment options The Plan offers a variety of investment options within the following categories or tiers:

1) target date investment options,

2) U.S. and foreign equity investments,

3) bond and stable value investments, and

4) ESG sustainable investment options.

You may select any one or combination of the investment options offered under the Plan. The default investment

option is the Vanguard Target Retirement Trust Select with the target year closest to the year you will reach age 65. You

can change your investment choices or move your existing account balance to different investment choices any time

(subject to frequent trading restrictions).

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

6

Starbucks Benefits Plan Description

|

search

Plan loans You can borrow up to 50% of your account balance, but no more than $50,000 (reduced by your highest outstanding

loan balance in the last 12 months).

The minimum loan amount is $500 and fees are assessed for each loan.

Two types of loans are permitted: General purpose loan (maximum 5-year loan) or primary residence loan (maximum

15-year loan).

You may have no more than one loan of each type outstanding at the same time.

Portability/rollovers You can transfer (roll over) your account to a new employer’s eligible retirement plan or an individual retirement

account (IRA) when you leave Starbucks.

You can roll over your account from another employer’s eligible retirement plan and/or an IRA into the Future Roast

401(k) any time after you are hired if you are on the Starbucks or a participating company’s U.S. payroll.

Tax savings Your 401(k) pre-tax and match accounts (including earnings) accumulate on a tax-deferred basis. No federal income taxes

are due until withdrawn. A 10% early withdrawal penalty may apply in some instances (generally applicable if you are under

age 59½ or if you are separated from Starbucks before age 55 and you take a distribution). You can continue to defer taxes

and avoid the early withdrawal penalty by rolling over your account balance to another employer’s eligible retirement plan

or a traditional IRA. Rollover from your pre-tax and match accounts to a Roth IRA will result in immediate taxation but the

early withdrawal penalty will not apply.

Roth after-tax contributions are made on an after-tax basis and are included in current taxable income. However, Roth

after-tax contributions, and, in certain cases, the earnings on those contributions, are not subject to income taxes when

distributed to you. In order for the earnings to be tax-free, the distribution must be a qualified distribution. A qualified

distribution is a distribution that is taken after you have had a Roth after-tax account in the Plan for at least five years and

after you have (a) reached age 59½, (b) become disabled, or (c) died. In applying the five-year rule, you count from January

1 of the year your first Roth after-tax contribution was made to the Plan (or, if earlier, to another eligible employer plan if

such amount was directly rolled over into this Plan). For example, if you make your first Roth after-tax contribution to the

Plan on November 30, 2022, your five-year period will end on December 31, 2026. It is not necessary to make Roth after-tax

contributions in each of the five years.

While amounts held in your Plan accounts must be paid out during your lifetime (generally starting after

age 72), if you roll your Roth after-tax account out of the Plan and into a Roth IRA prior to that time, you will not be

required to take distributions from your Roth IRA during your lifetime. This means that your Roth amounts, including

any earnings on those amounts, can continue to be tax-free and distributions from the Roth IRA can be postponed until

after your death.

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

7

Starbucks Benefits Plan Description

|

search

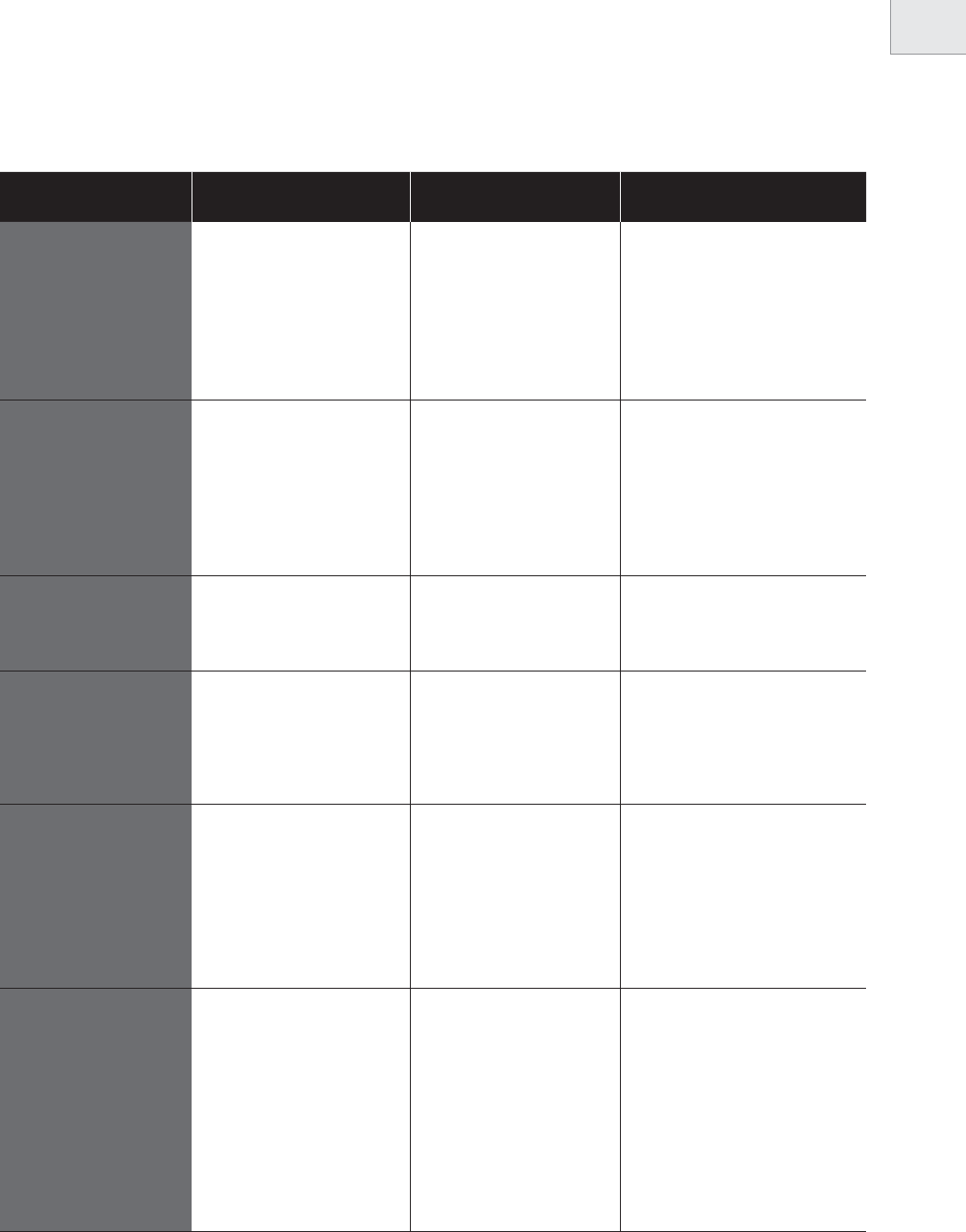

USING THE PLAN

Transaction When How Effective date

Enroll/start contributing Partners will be able to enroll

online or by phone starting

approximately 75 days prior to

attainment of eligibility

Go to netbenefits.com or

call Fidelity at (866) 697-1048

or (800) 587-5282 (Spanish line),

weekdays 530 a.m. to 9 p.m.

Pacific Time

Payroll contributions will start within

one to two pay periods after the later of

the date you enroll or the date you meet

the Plan’s eligibility requirements (90

days of employment, age 18 and on the

Starbucks or a participating company’s

U.S. payroll)

Starbucks Match The Starbucks Match is 100% of the

first 5% of eligible pay contributed

each pay period. This match rate is

in effect for future calendar years

unless changed by Starbucks.

The Starbucks Match is credited

to participants’ accounts

along with their 401(k) pre-tax

contributions and/or Roth

after-tax contributions

The Starbucks Match is deposited to

your account in the Plan as soon as

administratively possible after each pay

period in which you make 401(k) pre-tax

contributions and/or Roth after-tax

contributions (subject to IRS limits)

Change or stop

contributions

Any time after you start making

401(k) pre-tax and/or Roth

after-tax contributions

Go to netbenefits.com

or call Fidelity

As soon as administratively possible

following the request (usually within

1 to 2 pay periods)

Roll over a pre-tax and/

or Roth after-tax balance

from another employer’s

eligible retirement plan or

an IRA

Any time after you are hired and are

on the Starbucks or a participating

company’s U.S. payroll

Go to netbenefits.com

or call Fidelity

As soon as administratively possible

Change investment

direction for future

contributions

Any time after you start making

401(k) pre-tax and/or Roth

after-tax contributions

Go to netbenefits.com

or call Fidelity

Professional management

of your Plan account is

available through Fidelity

Personalized Planning & Advice,

netbenefits.com/plan

The day you make the change online or

by phone (if before 4 p.m. Eastern Time

or by the daily market close); otherwise,

the next business day excluding NYSE

holidays

Change existing

investment elections;

rebalance or exchange

your current account

balances

Any time after you have a

rollover, 401(k) pre-tax and/or

Roth after-tax account balance

in the Plan (frequent trading

restrictions apply)

Go to netbenefits.com

or call Fidelity

Professional management

of the investments in your

401(k) account is available

through Fidelity Personalized

Planning & Advice,

netbenefits.com/plan

(optional fee-based advisory

service)

The day you make the change online or

by phone (if before 4 p.m. Eastern Time

or by the daily market close); otherwise,

the next business day excluding NYSE

holidays

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

8

Starbucks Benefits Plan Description

|

search

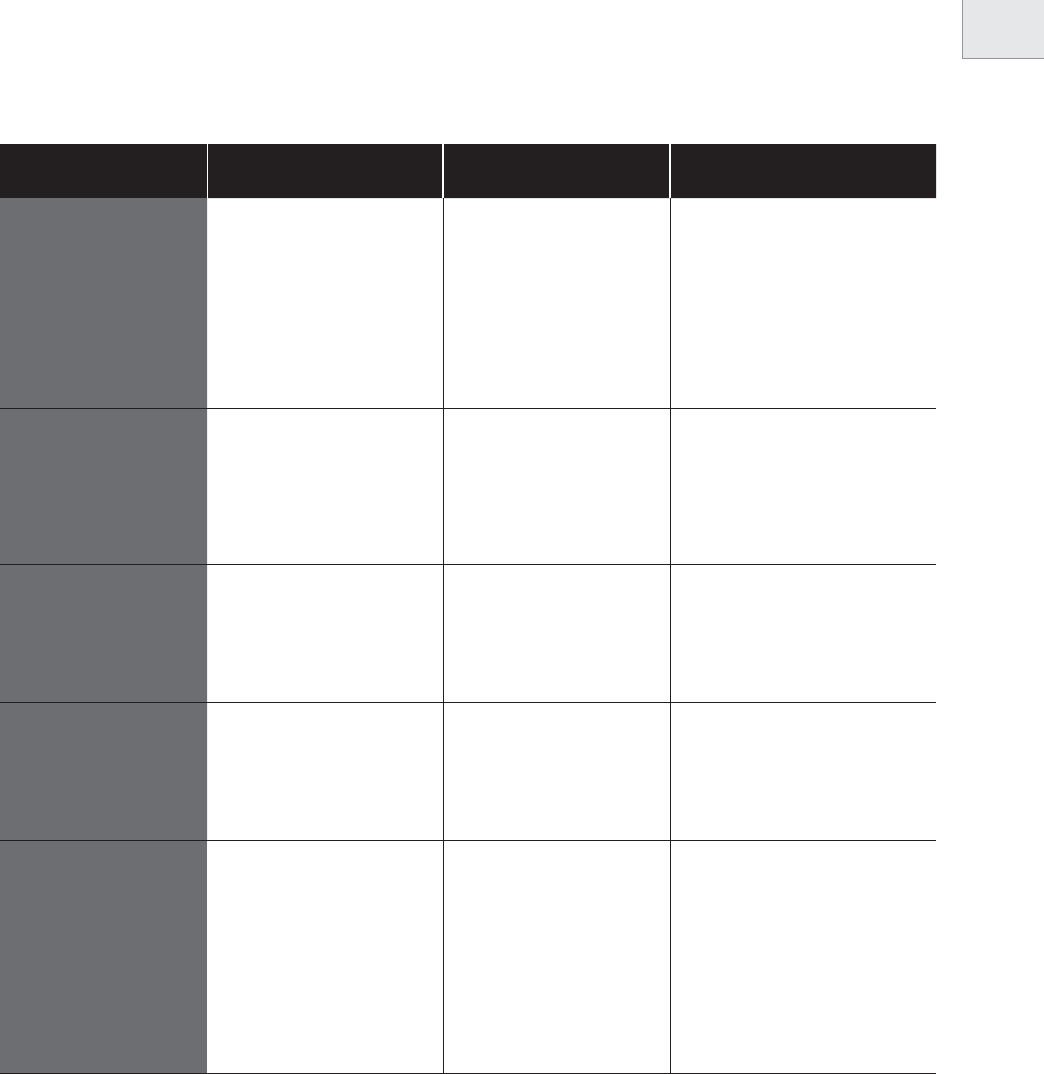

Transaction When How Effective date

Request a loan When your account balance is at

least $1,000

Go to netbenefits.com

or call Fidelity

General purpose loan – a check is

generally mailed or via EFT 3-5 business

days after your loan request is processed

Residential loan – application paperwork

mailed to you; check is generally mailed or

via EFT 3-5 business days after request is

received in good order

Request an age 59½

withdrawal

Annually from your 401(k)

pre-tax and/or Roth after-tax

account if you have attained at

least age 59½ and you are

actively employed

Go to netbenefits.com

or call Fidelity

A check is generally mailed or via

EFT 3-5 business days after request

is processed

Request a rollover account

withdrawal

Annually from your pre-tax rollover

account and annually from your

Roth after-tax rollover account if

you are actively employed

Go to netbenefits.com

or call Fidelity

A check is generally mailed or via

EFT 3-5 business days after request

is processed

Request a hardship

withdrawal

When you qualify for and apply for

a hardship withdrawal due to an

immediate, heavy financial need

(as defined in the Plan document).

Go to netbenefits.com

or call Fidelity

Hardship withdrawals are generally

processed within one business day

and mailed or sent via electronic funds

transfer the next business day

Request a final distribution When you leave Starbucks and any

related company for any reason,

you may take a distribution of

your account (in a lump-sum,

partial withdrawal or installment

payments) or roll over your account

into another employer’s eligible

retirement plan or into an IRA

Go to netbenefits.com

or call Fidelity

As soon as administratively possible

after Fidelity has been notified of your

separation, usually within 2-4 weeks

after your change in status

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

9

Starbucks Benefits Plan Description

|

search

FUTURE ROAST 401(k)

The Starbucks Future Roast 401(k) Savings Plan (also referred to in this chapter as the “Future Roast 401(k)” or

the “Plan”) can help you build financial security for your retirement and future needs. Through Future Roast

401(k), you can save part of your eligible pay before it is taxed for federal (and in most cases state) income

taxes (referred to as your “401(k) pre-tax contributions”). You can also elect to save part of your eligible pay

after it has been taxed for federal and state income taxes (referred to as your “Roth after-tax contributions”).

The amount you save is subject to FICA taxes. Plus, Starbucks matches a portion of your 401(k) pre-tax and/or

Roth after-tax contributions each pay period. See the section titled Contributions to Your Future Roast 401(k)

Account on page 13 for more details about matching contributions.

You decide how your entire Future Roast 401(k) account is invested among a variety of available investment

funds. You do not pay federal (and in most cases state) income taxes or penalties on the pre-tax money in

your Future Roast 401(k) account until it is distributed to you. If you timely roll your pre-tax account balance

into a traditional IRA or another employer’s eligible retirement plan when you separate from Starbucks and

any related company, you can continue to defer income taxes on your pre-tax account balance. Distributions

of your Roth after-tax contributions are tax- free. However, distribution of the earnings on those contributions

will be subject to income tax unless they are part of a qualified distribution. A qualified distribution is one that

is taken after you have had a Roth after-tax account in the Plan for at least five years and after you have (a)

reached age 59½, (b) become disabled, or (c) died. In applying the five year rule, you count from January 1 of

the year your first Roth after-tax contribution was made to the Plan (or, if earlier, to another eligible employer

plan if such amount was directly rolled over into this Plan). For example, if you make your first Roth after-tax

contribution to the Plan on November 30, 2022, your five-year period will end on December 31, 2026. It is not

necessary to make Roth after-tax contributions in each of the five years.

This chapter serves as the summary plan description (SPD) for the Future Roast 401(k) and summarizes the

Plan’s most important provisions as in effect on October 1, 2022. It applies to employees of Starbucks and

any participating company (as defined on page 45) who are eligible on or after that date. If your

employment with Starbucks or a participating company has terminated, portions of this SPD may not apply

to you. Within the SPD, references to “Starbucks” is intended to include Starbucks and any participating

company. Generally, your rights to benefits are governed by the terms of the Plan as in effect at the time your

employment terminated.

Please keep in mind that this SPD is only a summary of the principal features of the Plan. Although every

effort has been made to make this SPD as complete and accurate as possible, it is not a substitute for the Plan

document itself. The detailed provisions of the Plan document, not this SPD, govern the administration of the

Plan and the actual rights and benefits to which you are, or may become, entitled. Accordingly, in case of any

conflict between this SPD and the terms of the Plan document, the Plan document will control.

Este folleto contiene un resumen en inglés de los derechos y beneficios de su plan conforme al Plan de Ahorro

401(k) Starbucks Future Roast. Si tiene problemas para entender cualquier apartado de este folleto, envíe sus

preguntas a [email protected]. También puede escribirle a la Sra. Lisa Coutts, Savings and Retirement

Plan Administrator, Starbucks Corporation, 2401 Utah Ave S., MS: HR-3, Seattle, WA 98134. Asimismo, puede

llamar al despacho de la administradora del plan al (888) SBUX-411 or (888) 728-9411 para solicitar ayuda.

Horarios de atención: de lunes a viernes, de 7:30 a.m. a 4:30 p.m., hora del Pacífico.

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

10

Starbucks Benefits Plan Description

|

search

WHY SAVE IN FUTURE ROAST 401(k)?

The Future Roast 401(k) offers several important advantages over typical savings accounts:

• Your taxable pay is reduced because your 401(k) pre-tax contributions are not subject to federal and, in

most cases, state income taxes until they are withdrawn.

• While Roth after-tax contributions are made on an after-tax basis, any earnings are tax-free if they are

part of a qualified distribution.

• If you meet the eligibility requirements and contribute to the Plan, you will share in the Starbucks Match.

The Starbucks Match is contributed each pay period when you make 401(k) pre-tax contributions and/or

Roth after-tax contributions from your eligible pay

1

.

• Your 401(k) pre-tax contributions and any Starbucks matching contributions — plus any earnings — are not

subject to federal (and in most cases state) income tax until you take a distribution of your account balance

without timely rolling it over.

• You may be eligible for a federal tax credit on your tax return of up to 50% on the first $2,000 you

contribute ($4,000 if married filing jointly) to Future Roast 401(k) (certain income limits apply). For more

information about this special tax credit, see Tax credit for eligible savers on page 16.

Future Roast 401(k) is completely portable — meaning you can take your money with you if you are no longer

employed by Starbucks and any related company. If you withdraw your account balance upon your separation,

the taxable portion of your distribution may be subject to 20% mandatory withholding and possibly a 10%

early withdrawal penalty. Upon your separation, you may also be able to roll over (transfer) your account

balance into another employer’s eligible retirement plan, such as a 401(k) plan, 403(b) plan or 457 plan, or to a

traditional or Roth individual retirement account (IRA). Except for a rollover of your pre-tax balance into a Roth

IRA, when you roll over your Future Roast 401(k) account to another eligible retirement plan, you postpone

paying federal (and in most cases state) income taxes on your pre-tax money until required by the IRS (i.e.,

upon withdrawal or age 72 required minimum distribution payout). See Paying income taxes on page 35

for more information.

ELIGIBILITY

In general, you are eligible to contribute to Future Roast 401(k) if you satisfy each of the following conditions:

• Are on the Starbucks or a participating company’s U.S. payroll

• Are at least age 18, and

• Have completed 90 days of employment with Starbucks or any related company.

Different eligibility requirements may apply if you are employed by an entity that was recently acquired. See

Special eligibility rules for employees of acquired companies on page 11 for more information.

You are not eligible to contribute to Future Roast 401(k) if you are:

• Under age 18,

• Covered by a collective bargaining agreement, unless your bargaining agreement provides for participation

in Future Roast 401(k),

• Treated by Starbucks as an independent contractor or consultant,

• Leased as an employee from another company,

• Not on the Starbucks or a participating company’s U.S. payroll — such as a nonresident alien with no

U.S. source of income,

1 The maximum amount of eligible pay that will be taken into consideration when calculating 401(k) pre-tax and/or Roth after-tax

contributions and the Starbucks Match for any calendar year is subject to IRS limits ($305,000 for calendar year 2022).

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

11

Starbucks Benefits Plan Description

|

search

• Assigned to work overseas or in a foreign country permanently or indefinitely, or

• Not classified by Starbucks as an employee even if it is later determined that you were an employee.

A participating company is one that is wholly owned or partially owned by Starbucks Corporation and that has

adopted Future Roast 401(k) for its eligible partners.

If you are rehired

If you leave before 90 days of employment and are rehired

If you leave Starbucks and any related company before you have completed 90 days of employment and

are rehired within 12 months of leaving Starbucks and any related company, your time away counts toward

the 90-day eligibility requirement. If you are rehired after 12 months of leaving Starbucks and any related

company, your time away does not count for service credit. However, you still receive credit for the days

you had originally worked. Special rules may apply if you were separated from Starbucks or a participating

company for more than five years.

In certain circumstances, if you enroll prior to your eligibility date and subsequently separate employment

and rehire within 30 days of your date of termination, your prior enrollment election will apply to your future

eligible pay until changed by you. This 30-day period may be longer depending on your actual rehire date and

processing dates. If you believe this situation applies to you, you may contact Fidelity for confirmation of your

election status or to make another election.

Please contact the Starbucks Savings team via email at [email protected]om for more information.

Special eligibility rules for employees of acquired companies

Certain prior service for acquired companies is counted for purposes of eligibility as follows:

• Pasqua Coffee — Prior service counted for partners who were employed by Pasqua Coffee on March 1, 1999.

• Tazo, LLC — Prior service counted for partners who were employed by Tazo, LLC on January 20, 1999.

• Tympanum, Inc. (Hear Music) – Prior service counted for partners who were employed by Tympanum, Inc.

on October 18, 1999.

• Seattle’s Best Coffee LLC and Torrefazione Italia LLC – Prior service counted for partners who were

employed by Seattle’s Best Coffee LLC or Torrefazione Italia LLC on July 14, 2003.

• Coffee Equipment Company — Prior service counted for partners who were employed by Coffee

Equipment Company on or before April 1, 2008.

• Evolution Fresh — Prior service counted for partners who were employed by Evolution Fresh, Inc. on

November 10, 2011.

• Bay Bread, LLC and The New French Bakery, Inc. — Prior service counted for partners who were employed

by Bay Bread, LLC or the New French Bakery, Inc. on January 1, 2013.

• Teavana — Prior service counted for partners who were employed by Teavana Corporation on March 8, 2013.

If you are rehired and were previously eligible

If you left Starbucks and any related company after meeting the Plan’s eligibility requirements, you may be

immediately eligible to begin contributing to Future Roast 401(k) upon your rehire by a participating company.

Special rules may apply if you were separated from Starbucks or a participating company for more than five

years and in certain other situations. Please contact the Starbucks Savings team via email at

[email protected]om for more information if this applies to you.

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

12

Starbucks Benefits Plan Description

|

search

ENROLLING IN FUTURE ROAST 401(k)

You can enroll starting approximately 75 days prior to attainment of eligibility. Your payroll contributions will

start within one to two pay periods after the later of the date you enroll or the date you meet the Plan’s eligibility

requirements (90 days of employment, age 18 and on the Starbucks or a participating company’s U.S. payroll).

Participants will receive information from Fidelity containing enrollment instructions and Plan information

utilizing your email address and/or home address on file with Starbucks before you are expected to meet

the eligibility requirements and if you have not yet enrolled. If you meet the eligibility requirements and

you do not receive enrollment instructions from Fidelity, contact the Starbucks Savings team via email at

[email protected]om. You will need your Social Security number (Customer ID) in order to set up your

Personal Identification Number (PIN) when you enroll via the NetBenefits

SM

website or by phone. If you

already have an account with Fidelity, you will use the same Customer ID and PIN to enroll.

To enroll:

• Go online via the NetBenefits

SM

website at netbenefits.com 24 hours a day, seven days a week

• Speak with a Fidelity representative at (866) 697-1048 or (800) 587-5282 (Spanish line), weekdays from

5:30 a.m. to 9 p.m. Pacific Time, or

• Go to the Partner Hub under “Stock and Retirement Plans” on the Benefits tab. Click on “Future Roast

401(k)” to access Plan information and to link to NetBenefits

SM

to enroll.

Once you have completed your Future Roast 401(k) enrollment, your elections generally take effect within two

paychecks after the later of the date you meet the Plan’s eligibility requirements or the date you enroll.

Beneficiary designations

When you enroll, you must name one or more beneficiaries for your Future Roast 401(k) account. Your

beneficiary receives your account balance if you die. If you are married, your spouse is automatically your

beneficiary unless your spouse agrees in writing, with a notarized consent, to name another beneficiary.

Your spouse for purposes of Future Roast 401(k) means your “spouse” for federal income tax purposes.

Review, designate or change your beneficiary information online by accessing the NetBenefits

SM

website at

netbenefits.com, or by speaking with a Fidelity Representative at (866) 697-1048 or (800) 587-5282 (Spanish

line) to request a beneficiary designation form. If, at the time that you make your beneficiary designation,

you confirm that you are legally married, a spousal consent form will automatically be mailed to you for your

spouse’s signature if you name someone other than your spouse as your beneficiary. Your properly completed

beneficiary designation will become effective once the spousal consent is received by Fidelity.

If you do not have a valid beneficiary designation at the time of your death (i.e., you do not name a beneficiary,

you improperly complete the beneficiary designation form, you didn’t obtain any required spousal consent

or your designated beneficiary predeceases you) your Future Roast 401(k) account balance will be distributed

based on the following “hierarchy” or order:

1) Your spouse at the time of your death will automatically be your primary beneficiary (if you are married at

the time of your death),

2) In the event no such spouse survives you, your children (including natural and adopted children) will be

entitled to equal shares,

3) In the event no such spouse or child survives you, your estate will receive the balance of your Future Roast

401(k) account.

Refer to the Death benefit on page 34 for more information.

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

13

Starbucks Benefits Plan Description

|

search

CONTRIBUTIONS TO YOUR FUTURE ROAST 401(k) ACCOUNT

Your account can include several types of contributions:

• Your 401(k) pre-tax and/or Roth after-tax contributions deducted from your paycheck,

• Starbucks matching contributions,

• Rollover contributions, including (but not limited to) pre-tax, Roth after-tax, and tax-exempt

Thrift Savings Plan (TSP) contributions that you rolled over into this Plan,

• Contributions from another 401(k) plan that was merged into this Plan,

• Qualified non-elective contributions,

• Qualified matching contributions, and

• Starbucks discretionary profit-sharing contributions.

401(k) payroll contributions

In general, you can contribute from 1% to 75% of your eligible pay to Future Roast 401(k) each pay period, in

a combination of 401(k) pre-tax and/or Roth after-tax contributions, up to the annual IRS limit, $20,500¹

for calendar year 2022. For partners age 50 or older in 2022, the IRS limit is $27,000¹. These additional

contributions for partners age 50 or older are called “catch-up” contributions. These limits apply to only your

401(k) pre-tax and Roth after-tax contributions (and not to any of the other types of contributions listed

above). For example, if you are age 45 and you make 401(k) contributions in calendar year 2022 totaling

$20,500 and you receive Starbucks Match of $5,000, you have not exceeded the limits. Your 401(k) pre-

tax contributions and/or Roth after-tax contributions are deducted from your pay and are credited to your

account at Fidelity. Note that "catch-up" contributions do not require a separate election. Based on your

contribution rate, and during any year in which you are at least age 50, your payroll contributions will simply

continue until you reach the higher IRS limit applicable to partners who are "catch-up" eligible.

Your 401(k) pre-tax contributions are deducted from your eligible pay before federal (and in most cases state)

income taxes are calculated and withheld. This means you defer paying income taxes on your 401(k) pre-tax

account balance until you withdraw it. Your Roth after-tax contributions are deducted each pay period from

your eligible pay after your income taxes are taken out. Therefore, your take home pay will be less if you are

making Roth after-tax contributions than it would be if you were making the same amount of 401(k) pre-tax

contributions. The annual IRS limit applies to your combined 401(k) pre-tax and Roth after-tax contributions

in the Plan, and your pre-tax and Roth after-tax contributions to all other retirement plans (e.g., other 401(k)

plans, 403(b) plans and 457 plans) during the calendar year. The maximum amount of eligible pay that will be

considered annually when calculating your 401(k) pre-tax contributions and/or Roth after-tax contributions

and Starbucks Match is $305,000¹ for calendar year 2022. Some additional contribution limits may apply,

depending on your contribution rate, pay or position. These limitations are described in more detail in the

following pages.

1 These IRS limits are subject to annual cost of living adjustments published by the IRS.

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

14

Starbucks Benefits Plan Description

|

search

Starbucks Match

The Future Roast 401(k) provides for a matching contribution (as described below and on the following page).

Eligible partners who contribute to Future Roast 401(k) will receive the Starbucks Match. For the 2022 calendar

year and for future calendar years (unless changed by Starbucks), the Starbucks Match is 100% of the first

5% of eligible pay contributed by eligible participants each pay period. For any pay period in which you don't

make 401(k) pre-tax or Roth after-tax contributions, including those pay periods in which your contributions

are suspended due to reaching an IRS or Plan limit, no Starbucks Match will be contributed. Starbucks Match is

referred to as “Safe Harbor Match” in your account at netbenefits.com.

Your contribution as percentage of eligible pay Starbucks Match - 100% of the first 5% of eligible pay per

pay period. Maximum match = 5%

1%

100% match

2%

3%

4%

5%

The Starbucks Match will be contributed along with each participant’s 401(k) pre-tax and/or Roth after-tax

contributions each pay period to his or her account. All Starbucks Match contributions are immediately 100%

vested. This means you own Starbucks Match contributions as soon as they are deposited to your account.

Eligible pay

Eligible pay¹ for purposes of determining your 401(k) pre-tax and/or Roth after-tax contributions, Starbucks Match

and Starbucks discretionary profit-sharing contributions is generally defined as your regular salary or wages,

overtime and cash bonuses (except sign-on bonuses). Excluded from eligible pay are (1) distributions from the

Management Deferred Compensation Plan and taxable distributions from an unfunded, nonqualified plan of

deferred compensation, (2) CUP Fund payments, (3) tips (except for digital tips), (4) allowances, (5) gifts and

awards (unless designated by Starbucks as includable in eligible pay at the time of the award), (6) severance pay,

(7) non-U.S. source income, (8) amounts paid after the first pay period following severance from employment,

(9) child day care scholarships, (10) short-term and long-term disability payments, (11) differential wage payments

p

aid to partners in qualified military service, (12) any compensation for services paid to a nonresident alien who

is not a participant, (13) any amounts that would not be payable in cash, and (14) any other items excluded from

eligible pay as provided by the Plan document.

401(k) pre-tax and/or Roth after-tax contributions to Future Roast 401(k) are deducted from your eligible

pay each pay period according to your enrollment election. These deductions typically begin as soon as

administratively possible after the later of the date you enroll or the date you meet the Plan’s eligibility

requirements (usually within one to two pay periods). You can change, stop and restart your contributions at

any time without penalty. Contribution changes typically occur within two paychecks of your request.

Exceeding IRS limits in a calendar year

Controls are in place to appropriately limit your combined 401(k) pre-tax and/or Roth after-tax contributions

under the Future Roast 401(k) each calendar year. These controls are set to the appropriate IRS limit applicable

to you based on whether you will attain at least age 50 during the calendar year. However, in the event your

total 401(k) pre-tax and/or Roth after-tax contributions to the Future Roast 401(k) for a calendar year exceed

1 The maximum amount of eligible pay that will be taken into consideration when calculating 401(k) pre-tax and/or Roth after-tax

contributions and the Starbucks Match for any calendar year is subject to IRS limits ($305,000 for calendar year 2022).

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

15

Starbucks Benefits Plan Description

|

search

the IRS dollar limit for that year, the excess amount (referred to as "excess deferrals") will automatically be

distributed to you, adjusted for gains or losses. Starbucks matching contributions relating to any returned

excess deferrals will be forfeited.

Excess deferrals may also occur if you participated in both the Future Roast 401(k) and in a retirement plan

such as a 401(k), 403(b) or 457(b) plan maintained by another employer in the same calendar year. In this

situation, the monitoring and determination of whether an excess has occurred is your responsibility. The

excess amount, adjusted for gains or losses, is subject to federal (and in most cases state) income tax (to the

extent the excess is not attributable to Roth after-tax contributions) and must be returned to you by April 15 of

the following year to avoid adverse tax consequences. If this situation applies to you:

• You will need to decide which plan you wish to designate as the plan with the excess amount. To designate

the Future Roast 401(k), contact Fidelity at (866) 697-1048 by March 15 following the calendar year in

which your excess deferrals were made and request the Return of Excess Contributions form. You may

also find this form on netbenefits.com or on Partner Hub, under Benefits, then Future Roast 401(k). Your

excess deferrals will be returned to you, adjusted for gains or losses, by April 15 following the calendar year

in which your excess deferrals were made. 401(k) pre-tax contributions will be returned before Roth after-

tax contributions unless you elect otherwise. Applicable federal (and state) income taxes on any pre-tax

amounts being returned to you will be withheld. Starbucks matching contributions relating to any returned

excess deferrals will be forfeited along with any related gains or losses.

• If you fail to request the distribution of your excess deferrals by March 15 (resulting in the inability for the

Plan to process this refund by April 15), the excess amount is prohibited from being distributed until the

rest of your account is distributed. In this instance, you may end up paying income tax on the pre-tax

portion of any excess twice – once in the year in which the excess deferrals were made and again when

such excess amount is actually distributed to you.

If you feel this situation may apply to you, please contact Fidelity directly at (866) 697-1048.

If you are considered a highly compensated partner (as defined below), you may be further limited in the

amount you can contribute to Future Roast 401(k) in the event the Plan does not qualify for Safe Harbor status

in any given year. You will be notified if this applies to you.

Highly compensated definition for 2022

Partners are considered by the IRS to be highly compensated employees (HCEs) in 2022 if

they earn more than $130,000 gross pay (excluding Management Deferred Compensation

Plan deferrals) in the prior calendar year (2021) or if they are more than a 5% owner of

Starbucks. This compensation threshold is determined annually by the IRS and may be

increased in future years based on inflation.

Your 401(k) pre-tax and/or Roth after-tax contributions to your Future Roast 401(k) account will automatically

be suspended during the plan year when your total Future Roast 401(k) contributions have reached the

maximum allowed by law or the Plan. Beginning with the first paycheck of the following plan year, your 401(k)

pre-tax and/or Roth after-tax contributions will automatically resume at the rate they were when they were

discontinued unless you elect otherwise.

Safe Harbor Plan qualification

In any year in which the Starbucks Match (Safe Harbor Match) is made and the Plan meets the requirements to

qualify as a Safe Harbor Plan, the Future Roast 401(k) will automatically pass the applicable nondiscrimination

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

16

Starbucks Benefits Plan Description

|

search

tests. This means that highly compensated partners will not have additional refunds or limits imposed on them

due to nondiscrimination test results for the applicable year.

Discrimination test annual limit

In any year in which Starbucks is required to test the Plan for compliance with IRS nondiscrimination

regulations, limits may be imposed on certain highly compensated partners or refunds may be required. The

nondiscrimination regulations place limits on the amount that highly compensated partners can contribute

to Future Roast 401(k) as compared to contributions by non-highly compensated partners. If the limits are

exceeded, the Plan may be required to return to certain highly compensated partners a portion of their 401(k)

pre-tax and/or Roth after-tax contributions (and associated earnings), called excess contributions, made

during the plan year. A portion of Starbucks matching contributions, if any, (and associated earnings) may also

be considered excess contributions. You will be notified if these limits apply to you.

As an alternative, Starbucks may choose to make a 100% vested qualified non-elective contribution to the

Plan to satisfy all or a portion of the nondiscrimination regulations. Such contribution will be allocated to any

or all of the members of the non-highly compensated group who have met the eligibility requirements as

determined by Starbucks in accordance with the nondiscrimination regulations.

Tax credit for eligible savers

In addition to the tax advantages of participating in Future Roast 401(k), by contributing to the Plan you may

be eligible to receive a federal tax credit called the Saver’s Credit. The Saver’s Credit is up to 50% of your Plan

contributions depending on your adjusted gross income on your federal tax return (certain income limits

apply). Since the Saver’s Credit is not a deduction, it is used to reduce your tax payment to the IRS dollar for

dollar. The Saver’s Credit applies to the first $2,000 you contribute ($4,000 if married filing jointly). Certain

plan distributions in the same year may offset or limit your Saver’s Credit. A taxpayer who is younger than 18, a

full-time student, or who is claimed as a dependent on someone else’s return is not eligible for the Saver’s Credit.

For more information, contact your tax advisor or financial planner.

Rollover contributions

If you participated in a prior employer’s eligible retirement plan or if you have an individual retirement account

(IRA), you may be able to roll over the taxable portion of your account in that plan or IRA into the Future Roast

401(k) as soon as you are hired at Starbucks. Your rollover account is always 100% vested and belongs to you.

You will need to select your investment options at the time of your rollover.

Amounts that you can roll over

1

include:

• Pre-tax balances from your previous employer’s eligible retirement plan, including a Code Section 401(a)

qualified plan, a federal Thrift Savings Plan, a Code Section 403(b) annuity contract, or a Code Section

457(b) eligible deferred compensation plan,

• Direct rollover of Roth after-tax contributions from your previous employer’s eligible retirement plan,

including a Code Section 401(a) qualified plan, a federal Thrift Savings Plan, a Code Section 403(b)

annuity contract, or a Code Section 457(b) eligible deferred compensation plan,

• Direct rollover of tax-exempt amounts in uniformed services accounts in the Thrift Savings Plan for

federal employees,

• Balances from a traditional IRA, including conduit, SEP and Simple IRAs,

• Eligible retirement plan distributions that you receive as a surviving spousal beneficiary or as an

alternate payee under a Qualified Domestic Relations Order (QDRO), and

1 Subject to change. Please refer to the current Rollover Contribution Instructions and Application for eligible rollover sources

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

17

Starbucks Benefits Plan Description

|

search

• Distributions from 403(a) annuity plans.

Some payments that are not eligible for rollover into Future Roast 401(k) include:

• Periodic payments made to you from a previous employer’s eligible retirement plan that are scheduled to

last over a period of 10 years or more,

• Required minimum distributions (usually due to reaching age 72 or retiring) from previous employers’

eligible retirement plans,

• Non-taxable distributions received from previous employers’ eligible retirement plans (i.e., distributions of

after-tax contributions — pay you put into a savings plan after you have paid income taxes on it),

• Amounts held in a Roth IRA or a Coverdell Education IRA,

• Hardship withdrawals,

• Distributions from retirement plans of foreign countries, and

• In-kind distributions of employer stock.

For more information about rollover contributions, or to request a rollover contribution form, log on to

NetBenefits

SM

at netbenefits.com, on Partner Hub or call Fidelity at (866) 697-1048 (or (800) 587-5282 for a

Spanish speaking representative).

Starbucks discretionary profit-sharing contributions

In any plan year, Starbucks may choose to make a profit-sharing contribution to Future Roast 401(k). Any profit-

sharing contribution is solely at Starbucks discretion.

Partners eligible to participate in Future Roast 401(k) are eligible for a profit-sharing contribution, even if they

have never enrolled in Future Roast 401(k) or are not currently making 401(k) pre-tax and/or Roth after-tax

contributions. However, discretionary profit-sharing contributions will only be allocated to partners who are

actively employed by Starbucks or any participating company on the last day of the plan year (December 31)

and to partners who terminated employment during the plan year due to death, disability or retirement at or

after age 65.

The amount of any profit-sharing contribution allocated to an eligible partner’s account will be a percentage

of the total profit-sharing amount allocated to Future Roast 401(k). The eligible partner’s percentage will be

determined by dividing the partner’s eligible pay by the total eligible pay of all eligible partners. Eligible pay,

for purposes of allocating profit-sharing contributions, is the same as eligible pay for purposes of determining

your 401(k) pre-tax and/or Roth after-tax contributions and calculating the Starbucks Match as described

in Eligible pay on page 14, and is subject to the annually indexed IRS compensation limit ($305,000 for

calendar year 2022).

If a profit-sharing contribution is approved, more information will be provided at the time the contribution is

made to participant accounts.

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

18

Starbucks Benefits Plan Description

|

search

INVESTMENT OPTION TIERS

The Future Roast 401(k) offers a variety of investment options under four different categories or tiers as

provided below. You may choose to invest your account balance in any one or combination of such

investment options.

Tier 1 - Target Date Retirement Investments

To help you meet your investment goals, the Plan offers target date investment options (with different

allocations of stocks, bonds, and short-term investments) that vary in risks and returns. The year in the trust

name refers to the approximate year (the target date) when an investor in the trust would retire. For instance,

if you were born in 1980, you might choose the 2045 Target Retirement Trust Select because that is the year in

which you will attain age 65 (retirement). The trust will gradually shift its emphasis from more aggressive

investments (stocks) to more conservative ones (bonds and short-term reserves) based on its target date.

Investment performance in a Target Retirement Trust Select is not guaranteed at any time, including on or after

the target date.

Each Target Retirement Trust Select is designed so that it can be selected as a single stand-alone age-

appropriate investment based on the participant's default date of retirement (although there is no

requirement for the participant to select it as his or her only investment under the Plan).

A Target Retirement Trust Select is not a mutual fund. It is a collective trust available only to tax-qualified

plans and their eligible participants. Investment objectives, risks, charges, expenses, and other important

information should be considered carefully before investing. The collective trust mandates are managed by

Vanguard Fiduciary Trust Company, a subsidiary of The Vanguard Group, Inc.

Tier 2 - U.S. and Foreign Equity Investments

The funds in this category primarily focus their investments in the stock of public companies of varying sizes.

Depending on the fund, the companies can be based in the United States or internationally. Both actively

managed funds and passively managed index funds are included in this tier.

Tier 3 - Bond and Stable Value Investments

The funds in this category primarily focus their investments in bonds and other debt instruments. Depending

on the fund, investments are predominantly issued in the U.S. and may include government, corporate, or

inflation-protected bonds. Both actively managed funds and passively managed index funds are included in

this tier.

Tier 4 - ESG Sustainable Investments

These options take into consideration ESG (Environmental, Social and Corporate Governance) factors along

with financial factors in their investment decision making process. Both actively managed funds and a

passively managed index fund are included in this tier.

By selecting a combination of investment funds from the various tiers above, you can create an investment mix

that best suits your investment goals, time horizon and tolerance for risk. Each fund has a different objective

and strategy.

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

19

Starbucks Benefits Plan Description

|

search

Tier 1 - Target Date Retirement Investments

Vanguard Target Retirement Income Trust Select

Vanguard Target Retirement 2020 Trust Select

Vanguard Target Retirement 2025 Trust Select

Vanguard Target Retirement 2030 Trust Select

Vanguard Target Retirement 2035 Trust Select

Vanguard Target Retirement 2040 Trust Select

Vanguard Target Retirement 2045 Trust Select

Vanguard Target Retirement 2050 Trust Select

Vanguard Target Retirement 2055 Trust Select

Vanguard Target Retirement 2060 Trust Select

Vanguard Target Retirement 2065 Trust Select

Vanguard Target Retirement 2070 Trust Select

Tier 3 - Bond and Stable Value Investments

PIMCO Real Return Fund Institutional Class

Dodge & Cox Income Fund Class X

Vanguard Institutional Total Bond Market Index Trust

Wells Fargo Stable Value Fund E

Tier 2 - U.S. and Foreign Equity Investments

Winslow Large Cap Growth Fund Class I

Vanguard Institutional 500 Index Trust

Boston Partners Large Cap Value Equity Fund Class D

William Blair Small-Mid Cap Growth CIT Class III

Goldman Sachs Small Cap Value Fund Class R6

Vanguard Small Cap Index Fund Institutional Shares

MFS International Equity Fund Class 4

Vanguard Institutional Total International Stock Market Index Trust

Tier 4 - ESG Sustainable Investments

Legal & General Future World Developed Climate Change CIT Class A

Hartford Global Impact Fund Class R6

Nuveen Core Impact Bond Fund Class I

The investment options listed above are current as of July 1, 2022 and are subject to change. You can find more

detailed information about the current investment options by visiting NetBenefits

SM

at netbenefits.com or by

calling Fidelity at (866) 697-1048 (or (800) 587-5282 for a Spanish speaking representative).

Your total account balance is affected by the performance of your Future Roast 401(k) investments.

The importance of diversifying the investment of your accounts

To help achieve long-term retirement security, you should give careful consideration to the benefits of a well-

balanced and diversified investment portfolio. Spreading your assets among different types of investments

can help you achieve a favorable rate of return, while minimizing your overall risk of loss. This is because market

or other economic conditions that cause one category of assets, or one particular security, to perform very well

often cause another asset category, or another particular security, to perform poorly. If you invest more than

20% of your savings in any one company or industry, your savings may not be properly diversified. Although

diversification is not a guarantee against loss, it is an effective strategy to help you manage investment risk.

In deciding how to invest your savings, you should consult your personal advisor and take into account all of

your assets, including any savings outside of the Plan. No single approach is right for everyone because, among

other factors, individuals have different financial goals, different time horizons for meeting their goals, and

different tolerances for risk.

It is also important to periodically review your investment portfolio, your investment objectives and the

investment options to help ensure that your savings will meet your goals. You are solely responsible for investment

decisions under the Plan. Refer to Responsibility for investment decisions on page 39 for more information.

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

20

Starbucks Benefits Plan Description

|

search

The Future Roast 401(k) default investment

If you are participating in the Plan but you did not choose specific investment options, the Plan automatically

invests your existing balance and future contributions in the “default” investment option unless and until you

make an investment choice. The designated default investment option is the Vanguard Target Retirement Trust

Select with the target year closest to the year you will reach age 65.

For more information

More information about all of the investment options available in the Future Roast 401(k) can be obtained:

• On NetBenefits

SM

via netbenefits.com by clicking on the “Investment Performance and Research” link

under “Quick Links.”

• By speaking with a Fidelity representative at (866) 697-1048 or (800) 587-5282 (Spanish line) weekdays

from 5:30 a.m. to 9 p.m. Pacific Time.

• By calling (866) 811-6041 to inquire about Fidelity

®

Personalized Planning & Advice, an optional fee-based

managed account advisory service, or by logging on to netbenefits.com/plan.

Things to consider

Starbucks cannot provide investment advice. Each individual has their own unique investment time horizon

and risk tolerance. It is important for you to review the prospectus, the descriptions of the investment options

offered within the Future Roast 401(k) and all other available materials and resources to help you make

well-informed choices. You can access this information as well as tools for helping you determine the right

investment mix based on your needs by logging on to netbenefits.com. Additionally, partners have access

to enroll in professional management of their Future Roast 401(k) investments through Fidelity

®

Personalized

Planning & Advice, a fee-based managed account advisory service. Go to netbenefits.com/plan for more

information.

All investing is subject to risk. Investments in bond funds are subject to interest rate, credit, and inflation risk.

Diversification does not ensure a profit or protect against a loss in a declining market.

Each individual should carefully consider their investment objectives, risk tolerance, and the expenses and

charges associated with any option before investing.

Valuing your Future Roast 401(k) account

When you and Starbucks contribute to your Future Roast 401(k) account and you direct this money into the

investment funds, these funds can earn interest, dividends and capital gains (generally referred to as earnings

or gains). Sometimes your investment funds will record losses. These gains and losses are determined and

applied proportionately to your account through a process known as valuation.

Your account will typically be valued every business day the U.S. stock and bond markets are open. The

gain or loss from each of your funds is calculated based on the change in value of the underlying securities

each fund owns and any additional income since the previous day’s valuation. Fund expenses – such as

management fees, brokerage and transaction costs – are then subtracted, and the net gain or loss is allocated

proportionately to the number of shares you hold in your account.

In addition to your investment fund value changes, your account value is adjusted for contributions,

withdrawals and loan repayments. On occasion, Starbucks may need to delay or temporarily stop daily

valuation for special activities, such as changing Plan record keeping or investment funds.

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

21

Starbucks Benefits Plan Description

|

search

Making your investment elections

Before making your investment choices, be sure to read the detailed fund descriptions and prospectuses

available through NetBenefits

SM

at netbenefits.com or by calling Fidelity at (866) 697-1048 or (800) 587-5282

for a Spanish speaking representative. Also refer to Responsibility for investment decisions on page 39.

You can choose to invest in any one or combination of the investment options offered under the Plan. Your

investment elections must be made in whole percentages and must add up to 100%. If you choose to invest

in the target date investment options, it is recommended that you select the option that is closest to the date

you will reach age 65, although it is not required.

If you fail to make a valid investment election when you enroll, your account will be invested in the default

investment option, which is the Vanguard Target Retirement Trust Select with the target year closest to the

year you will reach age 65. Any Starbucks Match and discretionary profit-sharing contributions (if any) are

invested in the same funds you elect for your 401(k) pre-tax and/or Roth after-tax contributions.

Making changes to your investment elections

As with all investment decisions, participants are encouraged to review their own specific goals and risk

tolerance prior to investing in any fund(s).

Future contributions

You can change your investment elections for your future contributions at any time. Your investment election

changes will go into effect and apply to contributions starting within one to two business days of your election.

Existing account balance

The Future Roast 401(k) allows participants to change the investment of their existing account balance by using

the following transfer options:

• Change Future Investment Elections

• Exchange One Investment

• Exchange/Rebalance Multiple Investments

Change Future Investment Elections: You may elect to choose how your future contributions will be invested.

Your contribution sources, i.e., pre-tax, Roth after-tax, rollover accounts, Starbucks Match, Pre-2011 match

are all invested the same way, with the investment fund choices and percentages applied based on your

investment election.

Exchange One Investment: The exchange feature allows you to move a specific dollar amount or specific

percentage of a single fund to one or more funds. Exchanges are allowed at any time; however, there are

certain limitations and restrictions. For more information on Fidelity’s frequent trading policies, see

Frequent trading on page 23.

Exchange/Rebalance Multiple Investments: The rebalance feature allows you to change the allocation of your

existing account balance among the investment options on a percentage basis. When rebalancing, you would

consider your entire account balance and determine the percentage that you would like to invest in each

fund, so that in total 100% of your account balance is reallocated among the funds you choose. Rebalancing is

allowed at any time; however, there are certain limitations and restrictions. For more information on Fidelity’s

frequent trading policies, see Frequent trading on page 23.

Investment changes to your existing account balances received by stock market close (typically 1:00 p.m.

Pacific Time) will take effect the same business day. Investment changes received after market close will

transact the next business day. Investment changes you make to your existing account balances will apply

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

22

Starbucks Benefits Plan Description

|

search

to all your Future Roast 401(k) accounts, including any merged plan account and discretionary profit-sharing

contribution account.

You may make separate investment elections for your core accounts, which include your 401(k) pre-tax, Roth

after-tax and matching accounts (i.e. Match (pre-2011) and Safe Harbor Match) including earnings. Separate

investment elections may also be made for any rollover accounts including any pre-tax rollover account, Roth

after-tax rollover account and tax-exempt TSP rollover account.

How to make a change

You can make investment option changes, obtain additional information including fund performance and

expense and fee information, or access updated information about your Future Roast 401(k) accounts by:

• Logging on to NetBenefits

SM

at netbenefits.com.

• Calling Fidelity at (866) 697-1048 (or (800) 587-5282 for a Spanish speaking representative), weekdays

5:30 a.m. to 9 p.m. Pacific Time.

• You can also access NetBenefits

SM

via the Partner Hub under “Stock and Retirement Plans” on the Benefits

tab. Click on “Future Roast 401(k)” to access Plan information and to link to NetBenefits

SM

to enroll. Or log

into mysbuxben.com and click on the “Other Benefits” tab on the top, then click on “Your 401(k) or

Bean Stock” to link to NetBenefits

SM.

Partners can elect to enroll in professional management of their Future Roast 401(k) investments

through Fidelity

®

Personalized Planning & Advice, a fee-based managed account advisory service. Go to

netbenefits.com/plan for more information.

MANAGING YOUR ACCOUNT

You can request the following transactions online via NetBenefits

SM

at netbenefits.com or by contacting

Fidelity at (866) 697-1048 (or (800) 587-5282 for a Spanish speaking representative):

• Review your account balances.

• Review, increase or decrease your contribution percentage rate.

• Review fund information.

• Review or change your investment choices.

• Exchange or rebalance your account balances among the available investment funds.

• Designate your beneficiary.

• Manage a rollover.

• Request a loan.

• Request a hardship withdrawal.

• Request an in-service non-hardship withdrawal (i.e., age 59½ or rollover account withdrawal)

• Request a distribution following disability or separation from employment.

You can also review a summary of Future Roast 401(k) provisions by accessing “Plan Information and

Documents” under “Quick Links” on NetBenefits

SM

at netbenefits.com.

Account statements

Each quarter, Fidelity will make available a Future Roast 401(k) account statement online at netbenefits.com.

You will receive notification from Fidelity via email or postcard about the availability of your statement online.

The statement details all activity and investment results for your account during the quarter. You can also go

online via NetBenefits

SM

at netbenefits.com and elect to receive a paper statement of your Future Roast 401(k)

account at any time.

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

23

Starbucks Benefits Plan Description

|

search

Frequent trading

Future Roast 401(k) has a long-term objective: to help you build enough savings for you to live on when you

stop working. While you can transfer your Future Roast 401(k) account balance among the available investment

options on any business day, neither the Plan nor its investment options were designed for frequent trading.

Frequent or “excessive” trading is the purchase and subsequent sale (or vice versa) of a mutual fund within a

short period of time. Short-term and other excessive trading by shareholders can adversely affect a fund’s

performance by disrupting the portfolio manager’s investment strategy, by increasing expenses (such as

trading commissions) or by allowing some investors to capitalize on stale pricing at the fund’s expense.

To help protect the interests of fund investors who are seeking long-term returns on their investments, Fidelity

monitors excessive trading and limits the number of times investors exchange in and out of its funds, as well as

other investment products offered as options in workplace retirement plans as directed by the fund managers

or sponsors of the retirement plans.

Fidelity’s monitoring is based upon the concept of a “roundtrip” within a fund. In retirement plans, a roundtrip

transaction occurs when a partner exchanges in and then out (purchase and sale) of a fund option within

30 days. For the purposes of its excessive trading policies, purchases and sales do not include systematic

contributions or withdrawals (i.e., regular contributions, loan payments, hardship withdrawals) as permitted by

the Plan; they only include partner-initiated exchanges greater than $1,000.

Under Fidelity’s excessive-trading policies, partners are limited to one roundtrip transaction per fund within

any rolling 90-day period, subject to an overall limit of four roundtrip transactions across all funds over a

rolling 12-month period.

The first roundtrip in any fund results in a warning letter. Partners with two or more roundtrip transactions

in a single fund within a rolling 90-day period will be blocked from making additional purchases of the fund

for 85 days. Any four roundtrips in one or more funds in a 12-month rolling period will result in the partner

being limited to one exchange per quarter for 12 months. This applies to all investments subject to Fidelity’s

excessive trading policies. Once the 12-month exchange limitation expires, any additional roundtrip in any

fund in the next 12-month period will result in another 12-month limitation of one exchange per quarter.

Trading suspensions do not restrict a partner’s ability to make loan repayments, transact withdrawals from

Plan accounts, make investment exchanges out of the fund or continue to allocate employee and employer

contributions to the fund. In other words, the right to redeem (sell) is not affected by these policies, but the

ability to make subsequent exchanges into the fund will be.

Fidelity’s excessive trading limit and other short-term trading policies are subject to change by Fidelity.

Information about frequent trading restrictions and investment options including expenses and historical returns

is available at netbenefits.com in the “Investment Performance and Research” section under “Quick Links.”

Loans

Future Roast 401(k) is designed for long-term savings with a clear emphasis on planning for the future.

However, life sometimes involves pressing financial needs — short-term needs that may seem more important

than your long-term goals. That is why Future Roast 401(k) offers a loan option for partners who have a Future

Roast 401(k) account balance and are actively employed by Starbucks or a participating company at the time

the loan is taken.

When borrowing money from your Future Roast 401(k) account balance, there are no tax penalties (provided

you pay the loan back as scheduled), and the interest you pay goes right back into your own Future Roast 401(k)

||

back

page

}

|

page

main

contents

Future Roast 401(k)

Savings Plan

24

Starbucks Benefits Plan Description

|

search

account. In general, you may borrow up to 50% of your vested account balance up to a maximum of $50,000,

whichever is less. This amount will be reduced by your highest outstanding loan balance in the past 12 months.

When you take out a loan, you pay yourself back with interest. The interest rate is set at the time that you take

the loan and is the Wall Street Journal Prime Rate plus 1%. The current rate is available by calling Fidelity at

(866) 697-1048 (or (800) 587-5282 for a Spanish-speaking representative). The current interest rate is also

displayed when you model a loan on NetBenefits

SM

at netbenefits.com.

Future Roast 401(k) offers two types of loans: a general purpose loan and a primary residence loan. You can take

a general purpose loan for any reason for a maximum repayment period of five years. A primary residence loan

can only be obtained for the purchase of a home you are going to live in with a maximum repayment period of